“This reversal may mark the beginning of a more substantial reallocation of global funds towards Indian domestic themes,” said Vipul Bhowar, senior director and head of equities, Waterfield Advisors.

The main reason for the bullish outlook is the expected increase in earnings in the second half of fiscal year 2026, he said. Many companies are projected to see a 20–30% rise in profit after tax (PAT), fueled by strong festive-season sales and reduced raw material costs. While valuations may have limited upside, the earnings growth in these companies could surpass expectations, said Bhowar.

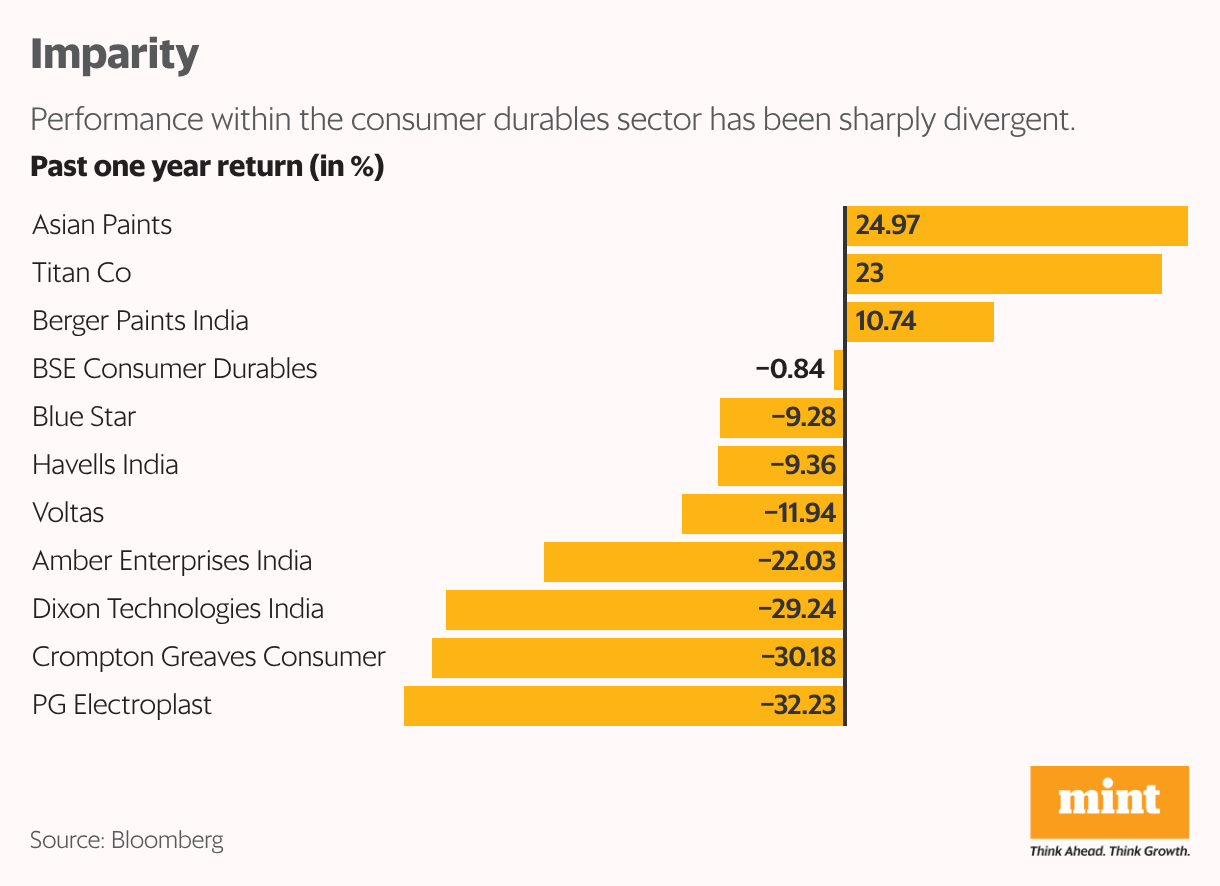

The renewed buying interest from foreign investors comes after the sector’s recent underperformance. The BSE Consumer Durables index fell about 1% over the past year, lagging the 12% rise in Nifty 50.

Performance within the sector has also been sharply divergent. Stocks such as Asian Paints, Titan Co. and Berger Paints India have gained between 11% and 25% over the past year, while the likes of Blue Star, Havells India, Voltas, Dixon Technologies India, Amber Enterprises India and PG Electroplast have declined 9-32%.

The recent reversal in FII flows into consumer durables This follows a sharp derating in sector valuations over the past six to seven months, said Manish Valecha, co-head of research, Anand Rathi Institutional Equities. He said that weak summer demand, subdued festive sales, and uncertainty around government approvals for key joint ventures, particularly those involving Chinese partners, have led to a meaningful compression of multiples and the removal of valuation froth.

While the sector continues to benefit from long-term structural tailwinds supported by recent government-led demand measures, including both direct and indirect tax cuts, the current FII buying appears more tactical in nature, according to Valecha.

“Investors are positioning for a relatively stronger H1CY26 versus H1CY25, which we believe is aided by a more favorable base and improved risk-reward at current valuations.”

Within the sector, according to Valecha, air conditioners and select electronics should see higher investor interest, driven by better growth prospects and stronger seasonality benefits.

budget optimism

Optimism linked to the Union Budget or interest-rate cuts is likely to be limited, given that tax cuts have already been announced and the RBI has been cutting rates over the past year, said Valecha. Incremental sentiment support, if any, could come from policy measures such as higher customs duties on imports of laptops and select electronic items, which could aid domestic manufacturing and improve competitiveness for local players, he said.

From a valuation perspective, Valecha said the upside from current levels appears meaningfully better than it did a year ago, although returns are likely to be more stock-specific rather than broad-based.

Barring a few names, most consumer durable stocks are trading below their long-term averages. For instance, Amber Enterprises India is currently valued at a price-to-earnings multiple of 84.84, lower than its five-year average of 94.72. Voltas is trading at 57.68 versus its five-year average of 109.53, while Havells is at 61.73 compared with a long-term average of 66.51.

In contrast, some stocks are trading at a premium. Asian Paints is currently valued at 75.79 times its earnings, higher than its five-year average multiple of 70.14, while PG Electroplast is trading at 55.50 versus its five-year average multiple of 52.36.

The investment thesis still faces risks, according to market participants. These include another weak summer, which could delay demand recovery; rising input costs, especially copper, which may hurt margins despite healthy volumes; and ongoing delays in government approvals for joint ventures, which could affect growth and profitability in the electronics segment.

Should the February 2026 budget fail to incorporate the anticipated personal income tax relief, Bhowar said the prevailing narrative of a “consumption boom” may begin to lose momentum.

If the US Federal Reserve postpones interest rate reductions until mid-2026, the strength of the dollar is likely to persist. According to him, this could trigger a new wave of FIIs engaging in “risk-off” selling in emerging markets.

Reading the Q3 picture

Electronic manufacturing services companies are expected to deliver moderate growth of about 11% in revenue, 17% in Ebitda and 11% in PAT in Q3 FY26, according to an 8 January report from Nuvama Institutional Equities. Appliance companies—across both large and small categories—are likely to see weak performance amid subdued consumption trends, it said.

“Among our coverage, Kaynes/Syrma SGS to post solid sales growth, followed by Polycab and KEI. Dixon, Havells, Crompton and Whirlpool to show a weak print,” Nuvama said.

Kotak Institutional Equities expects faster growth in wires and cables, driven by higher volumes, rising average selling prices due to sharp raw-material inflation, and a low base.

Room air conditioners may see a smaller decline, helped by some advance channel stocking, the brokerage said in a December 30 report. In the electronic consumer durables segment, growth in water heaters is likely to offset weakness in fans, while water and air purifiers are expected to see strong growth, it said.