Instead of a pharma company building its own factories and labs, which costs a lo, they hire a CDMO to handle everything from the initial drug chemistry to mass-producing the final pills or injections.

Advantage India

The nation has pivoted from being the “pharmacy of the world” (focused on cheap generics) to a global CDMO hub.

Here is why the Indian market is currently focused on this sector.

Cost-efficiency and skilled talent

India offers a significant cost advantage—often 30-50% lower than Western nations—without sacrificing technical expertise. The nation has one of the highest numbers of US FDA-approved manufacturing plants outside the US.

The “China Plus One” strategy

Global pharma giants are looking to diversify their supply chains to reduce reliance on China. India is the primary beneficiary of this shift, as companies seek stable, English-speaking, and legally compliant alternatives for drug development.

Government boosts

The Indian government’s production linked incentive (PLI) schemes are pumping money into the sector to encourage the manufacturing of “active pharmaceutical ingredients”—the raw materials that make drugs work.

As the industry thrives, here are 5 CDMO stocks that you can add to your watchlist.

This is not a stock recommendation.

Syngene International

The company is a global contract research, development and manufacturing organisation (CRDMO). Syngene International provides integrated scientific services to pharmaceutical, biotechnology, animal health, consumer goods, nutrition and speciality chemical companies worldwide.

The company’s clients include some of the world’s leaders in their fields, including top global multinationals.

On the financial front, in Q3FY26, revenue from operations declined 3% year-on-year to ₹917.1 crore. Operating Ebitda for the quarter stood at ₹209.0 crore, with a margin of 23%.

The net profits of Syngene International were placed at ₹15.0 crore vs ₹131.1 crore year-on-year.

A key factor impacting third-quarter performance was the ongoing impact from a single commercial-stage product for the largest large-molecule biologics customer.

Outside of this, the underlying business performance showed good progress.

During the third quarter, Syngene International incurred a total capital expenditure of around $9 million. Around 50% was invested in research services primarily across capability builds, including DMPK biology, ADC labs and contractual obligations in dedicated centres, along with regular expansion.

Moving ahead, the company has extended its partnership with Bristol Myers Squibb, which remains its largest client. The company is supporting Bristol Myers with over 700 scientists. The collaboration with Bristol Myers has been extended through to 2035.

Syngene International has also expanded its advanced chemistry capabilities at Hyderabad with new catalytic screening and flow chemistry laboratories.

The company has also commissioned a new commercial-scale facility for liquid-filled hard gelatin capsules, significantly enhancing its oral solid dosage platform.

At Syngene’s Bayview Biologics facility in the US, process and equipment validation are now complete, and hiring is underway to support operations as planned.

Overall, the company’s differentiated scientific capabilities, long-standing client relationships and diversified business model across research services and CDMO continue to provide resilience, balance, and growth.

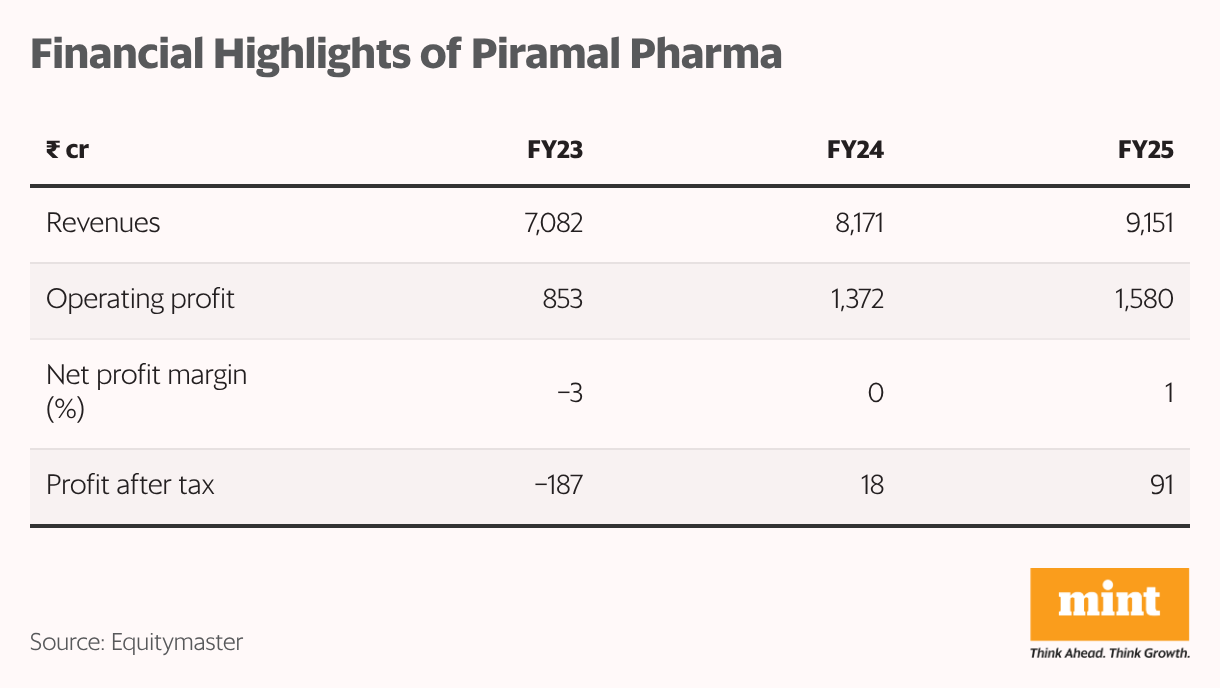

Piramal Pharma

Piramal Pharma is a top CDMO player. The company has 17 global development and manufacturing facilities and a global distribution network in over 100 countries.

Piramal Pharma includes Piramal Pharma Solutions (PPS), an integrated contract CDMO, Piramal Critical Care (PCC), a complex hospital generics business, and the India Consumer Healthcare business, selling over-the-counter products.

On the financial front, Piramal Healthcare’s Q3 FY26 revenues were at ₹2139.9 crore, down from ₹2,204.2 crore year-on-year. The company has been reporting losses for the last few quarters.

According to the company, revenue growth in Q3/9M FY26 was impacted by inventory destocking in one large on-patent commercial product by customer, slower early-stage order inflows in H1 FY26 due to inconsistent recovery in US biopharma funding, along with uncertainties on global trade policies, and regulatory delays in inhalation anaesthesia for ex-US markets from Digwal facility.

Despite lower revenues, impact on Ebitda was partly offset by the company’s efforts towards cost optimization.

Moving ahead, the company’s management says they are seeing a significant pick-up in RFPs with early signs of recovery in order inflows since October 2025 on the back of improved biopharma funding and increased M&A activities in the US.

Piramal Pharma’s growth capex of $90 million investment to expand Lexington and Riverview facilities is on track.

In the complex hospital generics (CHG) business, Piramal Pharma is investing in new products and expanding its presence in the ex-US markets.

The company acquired niche brand Kenalog, which is synergistic with its current business. Kenalog is a branded commercial injectable product with complex manufacturing requirements, complementing the CHG product portfolio.

According to management, the consumer business continues to outperform in its representative markets, with robust growth across its power brands.

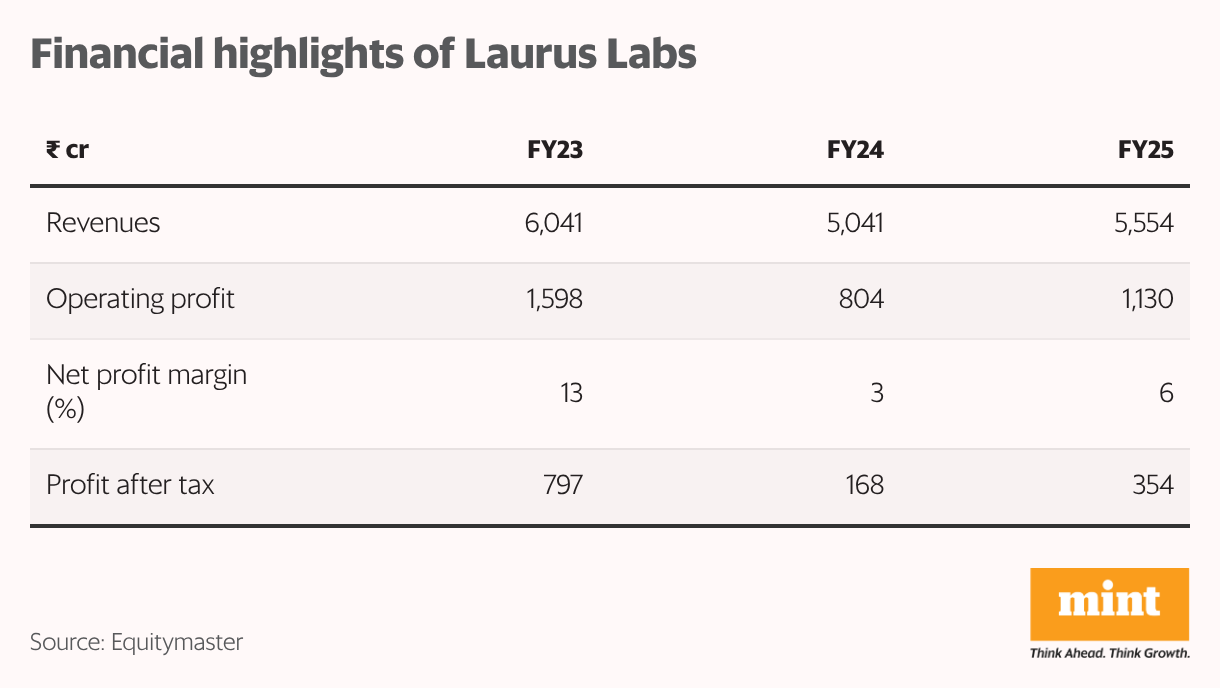

Laurus Labs

Laurus Labs holds a leadership position in developing and manufacturing select active pharmaceutical ingredients and finished dosage forms (FDF) across anti-retroviral, oncology, cardiovascular, and gastrotherapeutic.

The company offers end-to-end CDMO services, supporting innovators from early-stage development to commercial production. Laurus Labs operates 15 facilities approved by global regulators, including the USFDA, WHO, EMA, and others.

The company reported Q3 revenues of ₹1,778 crore, showing a 26% revenue growth year-on-year. The Ebitda was placed at ₹485.0 crore, reporting a solid 70% growth. The net profits of the company were placed at ₹2,53.1 crore vs ₹90.6 crore year-on-year.

Moving ahead, Laurus Labs has made significant investments in capex so far in peptide development and manufacturing infrastructure is concerned. This is to meet its current and future capacity requirements.

In addition, the company has operationalized its antibody drug conjugate and gene therapy process development labs in Hyderabad.

In terms of the construction of the new GMP manufacturing facility, it is well on track.

Late last year, Laurus Labs also announced an increase in joint investments in Krka Pharma, which is in line with its plan to support ongoing FDA facility construction in Hyderabad. Phase 1 is expected to be completed by mid-2027.

Overall, the company has shown strong recent financial growth, with rising revenues and margins, largely supported by growth in its contract development and manufacturing organization business. CDMO revenue has been growing rapidly and now accounts for a significant share of total sales.

Management expects CDMO to contribute around half of revenue in the medium term, which typically offers higher margins than traditional generics.

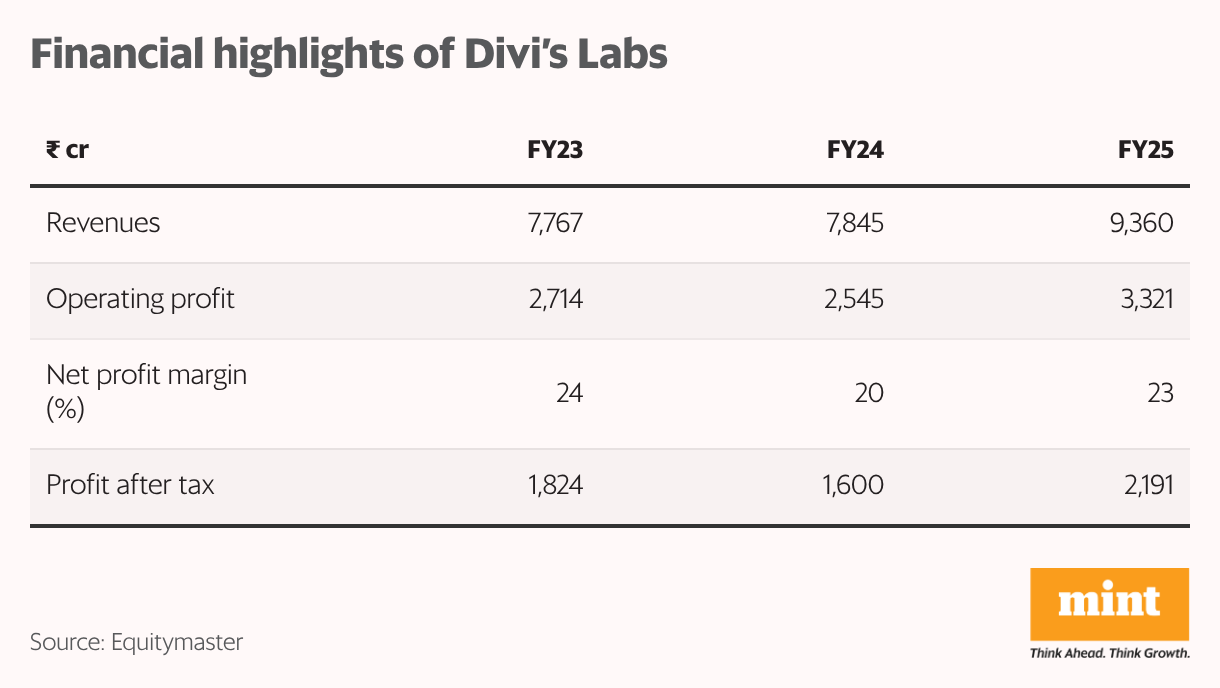

Divi’s Labs

The company is a leading manufacturer of high-quality API, intermediates, and registered starting materials, supplying to over 100 countries.

The company is ranked among the top 3 API manufacturers globally. Divi’s Labs operates three manufacturing facilities located near Hyderabad, Visakhapatnam, and Kakinada in India. Unit 2 in Visakhapatnam is well-known as the world’s largest API manufacturing facility.

On the financial front, Divi’s Labs achieved a consolidated total income of ₹2,860.0 crore in Q2 FY26, representing a 17% increase from ₹2,444.0 crore in the corresponding quarter of the previous financial year. Profit after tax for the quarter was placed at ₹689.0 crore against ₹510.0 crore in Q2 FY25.

Exports for H1 FY26 accounted for about 90% of total sales revenue. Exports to Europe and the US combined were about 73%.

In the generics business, the company maintained consistent volumes across its core portfolio, despite ongoing pricing pressures. The company’s backward integration continues to enable it to manage input costs effectively.

The Unit 3 facility in Kakinada, which became operational earlier in 2025, is supporting Divi’s Labs supply chain by enabling in-house production of starting materials and intermediates.

In the custom synthesis segment, the company continues to see high engagement levels with a steady flow of RFPs and site visits from global innovators.

The company currently has multiple projects advancing through development and validation stages. A few of them are expected to move into commercial manufacturing over the next 1-2 years.

In the peptide segment, management says they are seeing strong momentum in peptide synthesis. Divi’s Labs has recently inaugurated its peptide centre of excellence, where multiple projects of various customers are undergoing development.

The company is actively engaged with several big pharma companies at various stages in their phase I, phase II and phase III programs. As these programs advance through regulatory milestones, the company is preparing to further scale up investments to meet the demand.

Divi’s Labs is currently executing three major capex programs backed by long-term supply commitments. These investments are focused on implementing new technologies, expanding capacities and advancing key strategic projects.

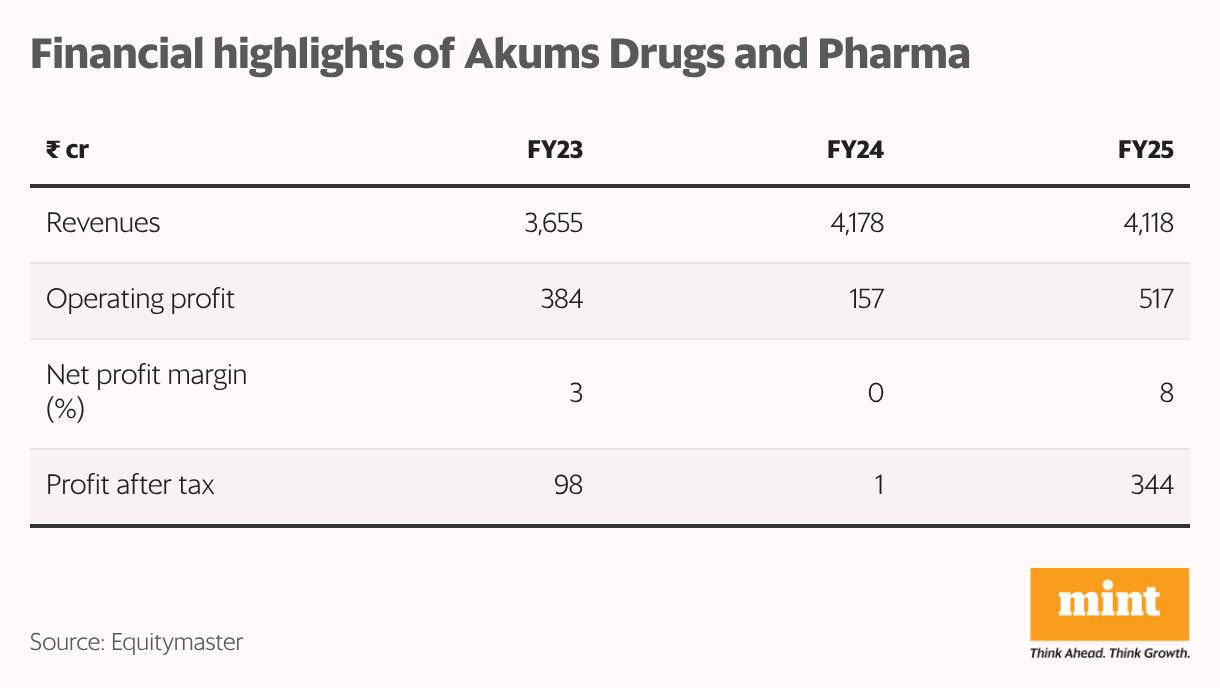

Akums Drugs and Pharmaceuticals

Next on our list is the stock of Akums Drugs and Pharmaceuticals (Akums Drugs and Pharma).

Akums Drugs and Pharma is India’s largest CDMO. The company has developed over 4,100 commercialized formulations across 60+ dosage forms.

It caters to therapeutic areas such as cardio-diabetes, neurology, gynaecology, nephrology, anti-infectives, respiratory, analgesics, and multi-vitamins.

On the financial front, the Q2 FY26 numbers were below expectations. Akums Drugs and Pharma saw revenues dip to ₹1,017.5 crore in Q2 FY26 from ₹1,033.1 crore year-on-year. Net profits of the company fell sharply to ₹42.7 crore from ₹66.7 crore year-on-year in the same period.

Post the Q2 FY26 numbers, the management highlighted the fact that during the quarter, margins saw a dip as API price continued their downward trend. According to the company, the downward spiral of API prices continues to be broad-based across all categories of APIs.

Moving ahead, the company has entered into a partnership with the government of the Republic of Zambia.

Accordingly, there would be a joint venture with the Zambian government to set up a manufacturing plant in Zambia. Akums Drugs will hold 51% in the joint venture.

The new facility is planned to be established in Lusaka, the capital city, and is anticipated to begin production in calendar year 2028.

Additionally, Akums Drugs and Pharma recently completed a European GMP audit for its Plant 2 in October 2025, with approval expected by the fourth quarter of this year.

On the export side, the company has successfully shipped its first commercial batch of Dapagliflozin tablets to Switzerland. A supply of Rivaroxaban tablets to Europe is also projected for the third quarter.

The European pipeline appears robust, featuring over ten active dossiers. Overall, Akums Drugs and Pharma shows significant potential with its Zambian joint ventures and ongoing export initiatives.

However, investors should remain mindful of potential pricing pressures in the API segment.

Should You Consider CDMO Stocks?

Pharma companies are increasingly outsourcing development and manufacturing, which creates a structural growth opportunity.

However, the sector is not without challenges. Pricing pressure is a key concern as competition among global and domestic CDMOs is intense, and large pharma clients have strong bargaining power, which can limit margin expansion.

Rising costs related to compliance, skilled manpower and capacity expansion also add pressure, especially if companies are unable to pass these costs on to customers.

Overall, CDMO stocks could make sense as a selective, long-term proposition, but investors should be cautious on valuations and focus on companies with strong execution, diversified clients and differentiated capabilities.

Investors should evaluate the company’s fundamentals, corporate governance, and valuations of the stock as key factors when conducting due diligence before making investment decisions.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com