Large numbers like these often unsettled investors. But seasoned market participants know that transaction promoters need context. Not every sale signals distress.

Even as overall promoter holdings across listed companies have trended lower, a quieter and more telling counter-trend has emerged. Some promoters have been buying shares from the open market, signaling conviction in their businesses at a time when uncertainty remains high.

These transactions are more than just disclosures. They reflect promoters putting fresh capital at risk, backing the upside they believe the market has yet to fully recognise.

If you would like to explore this theme further, you can join Richa Agarwal, Equitymaster’s smallcap editor, for an online discussion on promoter buying in Indian stocks.

We look at four recently listed companies where promoters have been increasing their stake through open-market purchases.

Enviro Infra Engineers

First on the list is Enviro Infra Engineers, a company specializing in end-to-end water and wastewater management solutions across India. It caters to both municipal and industrial clients, offering turnkey projects such as sewage treatment plants, sewerage systems, water treatment plants, water supply systems, and common effluent treatment facilities.

During the December 2025 quarter, the company’s promoters raised their stake to 70.13%.

Enviro Infra has delivered rapid growth, with sales and net profit compounding at 62% and 102% respectively over the past five years. Over the same period, its return on equity (ROE) and return on capital employed (ROCE) have averaged a strong 34% and 45%.

Looking ahead, the company expects revenue to grow by over 15% this year, while net profit is projected to rise by more than 20%. Its order book stands at around ₹20 billion, providing revenue visibility of nearly two years.

Government-led infrastructure spending remains a key tailwind. Enviro Infra plans to capitalize on schemes such as AMRUT 2.0, the Namami Gange Programme, the National River Conservation Plan, and the National Plan for Conservation of Aquatic Ecosystems.

The company is also expanding its geographic footprint to emerge as a pan-India player, while scaling up project sizes to improve margins.

Enviro Infra debuted on the markets in November 2025, with its IPO attracting an oversubscription of 91 times. Since listing, however, the stock has declined by about 8%.

Looking ahead, the company expects revenue to grow by over 15% this year, while net profit is projected to rise by more than 20%. Its order book stands at around ₹20 billion, providing revenue visibility of nearly two years.

Government-led infrastructure spending remains a key tailwind. Enviro Infra plans to capitalize on schemes such as AMRUT 2.0, the Namami Gange Programme, the National River Conservation Plan, and the National Plan for Conservation of Aquatic Ecosystems.

The company is also expanding its geographic footprint to emerge as a pan-India player, while scaling up project sizes to improve margins.

Enviro Infra debuted on the markets in November 2025, with its IPO attracting an oversubscription of 91 times. Since listing, however, the stock has declined by about 8%.

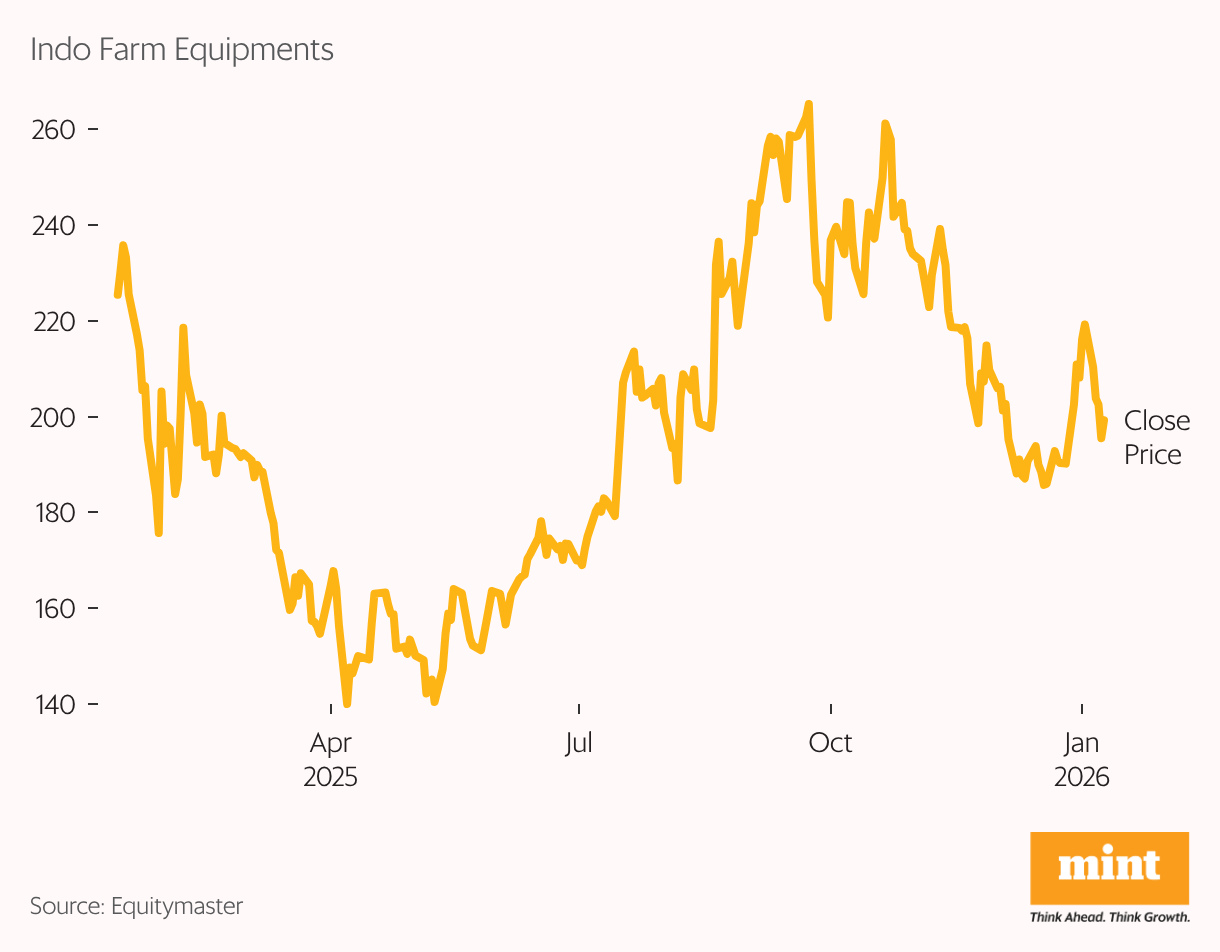

Indo Farm Equipments

Indo Farm Equipments manufactures and markets pick-and-carry cranes with capacities ranging from 9 to 30 tonnes, as well as mobile tower cranes.

The company also produces tractors, cranes, harvester combines, engines, and diesel gensets at its manufacturing facility in Baddi, Himachal Pradesh. Over time, Indo Farm has built a strong presence through an extensive dealer network.

Its installed capacity currently stands at 12,000 tractors and 1,280 cranes annually. Supporting its sales ecosystem is Barota Finance, an in-house NBFC that facilitates customer financing.

In the December 2025 quarter, promoters increased their stake to 69.53%.

Financially, Indo Farm has recorded a five-year CAGR of 10% in sales and 37% in net profit. However, its average return ratios remain modest, with ROE and ROCE of 5% and 11% respectively.

Nearly 95% of the company’s revenue comes from its tractor and mobile crane divisions. Tractor demand in India is influenced by multiple variables, including rural income and monsoon patterns, and any sustained improvement could materially lift volumes and margins.

The company is also expanding its international footprint, with overseas markets currently contributing about 10% of total revenue.

Indo farm raised ₹2.6 billion through its IPO in January last year. Since listing, the stock has declined by around 20%.

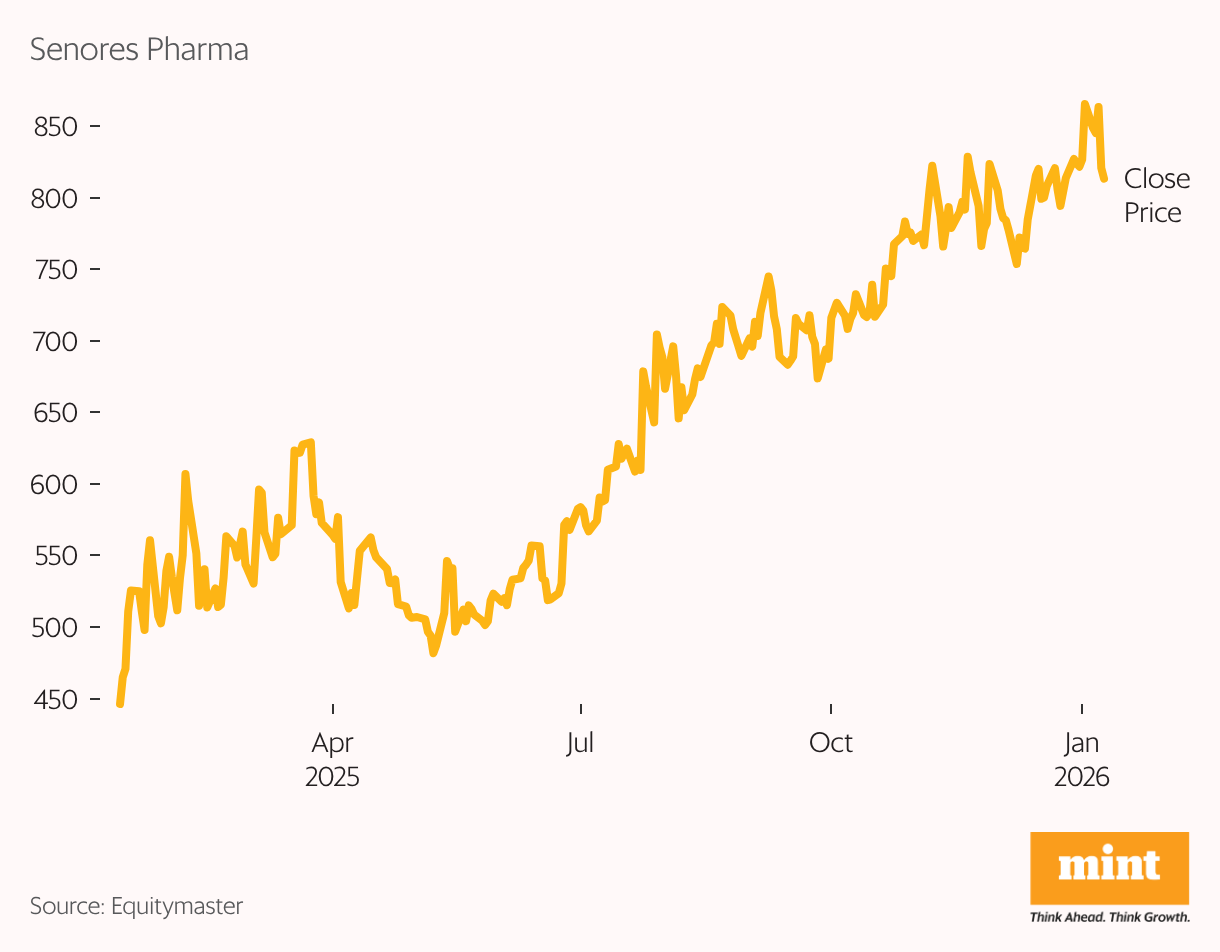

Senores Pharma

Senores Pharma is a research-driven formulations company with a strong focus on regulated markets such as the US, Canada, and the UK. These geographies account for over 60% of its revenue, with the US alone contributing nearly 70% of sales from regulated markets.

The company operates across multiple therapeutic areas, including infertility, cardiovascular, CNS, antidepressants, endocrine disorders, respiratory care, pain management, and oncology. In addition, it has exposure to over 40 emerging markets through branded generics.

Nearly 95% of the company’s revenue comes from its tractor and mobile crane divisions. Tractor demand in India is influenced by multiple variables, including rural income and monsoon patterns, and any sustained improvement could materially lift volumes and margins.

The company is also expanding its international footprint, with overseas markets currently contributing about 10% of total revenue.

Indo farm raised ₹2.6 billion through its IPO in January last year. Since listing, the stock has declined by around 20%.

Senores Pharma

Senores Pharma is a research-driven formulations company with a strong focus on regulated markets such as the US, Canada, and the UK. These geographies account for over 60% of its revenue, with the US alone contributing nearly 70% of sales from regulated markets.

The company operates across multiple therapeutic areas, including infertility, cardiovascular, CNS, antidepressants, endocrine disorders, respiratory care, pain management, and oncology. In addition, it has exposure to over 40 emerging markets through branded generics.

Promoter buying has been consistent, with the stake rising to 45.8% in the December 2025 quarter—marking the second consecutive quarter of purchases.

Over the past three years, Senores Pharma has delivered exceptional growth, with sales and net profit compounding at 204% and 289% respectively. Its average ROE and ROCE during this period stand at 14% and 13%.

Beyond its owned and acquired product portfolio, the company has built a presence in contract development and manufacturing (CDMO) and entered into marketing partnerships with global and domestic pharma players to scale its formulations business.

Management has guided for 50–60% topline growth and a doubling of net profit in FY26, driven by portfolio expansion, stronger branded generics performance, and improving profitability.

Senores Pharma listed in December 2024 after offering 14.9 million shares. The IPO comprised a fresh issue of 12.8 million shares worth ₹5 billion and an offer for sale of 2.1 million shares. Priced at ₹391, the stock debuted at ₹594.

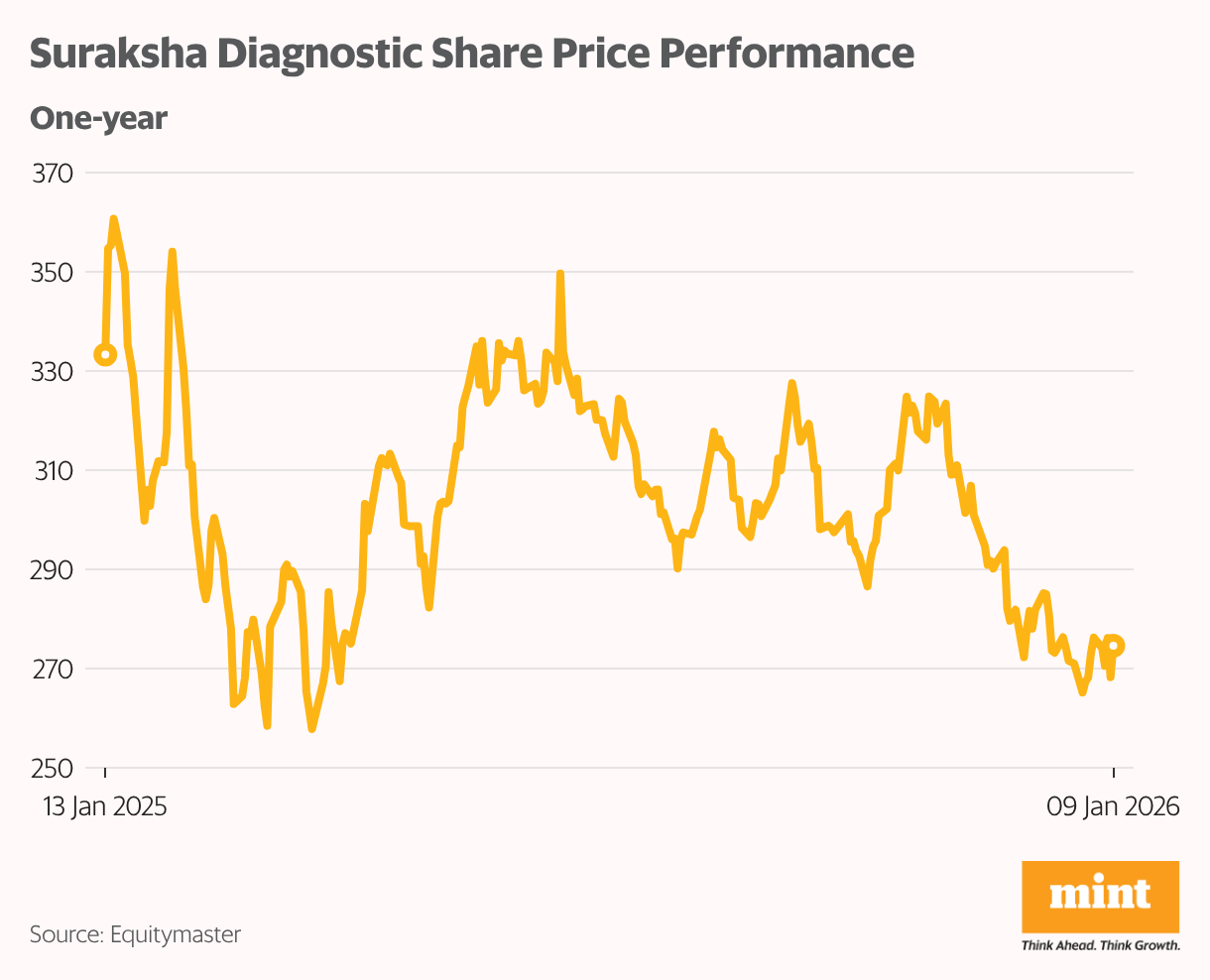

Suraksha Diagnostic

Suraksha Diagnostic, incorporated in 2005, is engaged in pathology, radiology, medical consultations, and genomics testing. It is among the largest diagnostic chains in Eastern India and operates on a hub-and-spoke model.

The promoters, who bring over three decades of industry experience, have built a network of more than 10,000 doctor partnerships. About 90% of the company’s revenue comes from walk-in customers, giving it a strong brand presence, particularly in West Bengal.

Promoter stake edged up again in the December 2025 quarter to 48.98%, following incremental increases in the previous two quarters.

Over the past five years, the company’s sales and net profit have grown at a CAGR of 10% and 15% respectively. Its average ROE and ROCE stand at 10.5% and 17%.

Suraksha is now pursuing inorganic growth through selective acquisitions of regional diagnostic centres. Recently, it acquired a 63% stake in Fetomat, a prenatal and fetal medicine clinic. It is also expanding its B2B segment by strengthening partnerships with hospitals and insurance providers.

The company raised about ₹8.5 billion through its December 2024 IPO, which was entirely an offer for sale.

What it signals

When promoters buy shares in their own companies, it often reflects confidence in long-term prospects—especially during periods of market volatility.

That said, promoter buying should not be viewed in isolation. While it can be a useful signal, investors must also assess fundamentals, governance standards, valuations, debt levels, industry dynamics, and broader market conditions before making investment decisions.

Disclaimer: This article is for information purposes only and should not be construed as investment advice.

This content is syndicated from equitymaster.com.