Tax revenues are the backbone of government finances, yet a significant portion of these revenues remains unrealized. When funds are locked up in legal and administrative limbo, it creates a fiscal drag that stifles public infrastructure and welfare initiatives.

Tax revenue raised but not realized stood at ₹38.4 trillion at the end of FY25—30.5% higher than last year. It has grown nearly 200% since the introduction of the Direct Tax Vivad se Vishwas Scheme in 2020.

However, FY23 marked a clear inflection point, with the share ‘tax not under dispute’ rising significantly following the government’s voluntary settlement schemes. Its share rose from less than 20% in FY20 to more than 50% by FY25.

While this marks a shift towards reducing pending income tax litigation, providing resolution to both taxpayers and government, ‘tax under dispute’ has stayed elevated—rising 16.2% year-on-year in FY25. To put the number in context, tax under dispute increased by ₹2.5 trillion, which is about 6.6% of the ₹₹38 trillion in gross tax collections for FY25.

Experts noted Vivad Se Vishwas Scheme played a major role in reducing disputes. The first round of the scheme settled almost ₹1 trillion in disputed direct taxes across over 130,000 cases, according to finance ministry data. A second scheme was launched in 2024.

“Faceless assessments and appeals have reduced jurisdictional bias and improved the quality of assessments to some extent (leading to fewer disputes),” said Aditi Goyal, partner, tax practice, at Trilegal.

While there are signs of a progressive compositional shift, experts are still cautious since the amount under dispute has kept rising. “The tax which is not under dispute has increased sharply, which makes the disputed amount appear smaller in relative terms. However, in absolute terms, the tax under dispute has not declined,” said Sandeep Bhalla, partner at Dhruva Advisors.

In Budget 2026, the government announced more measures to ease tax compliance. These include simpler filings, longer deadlines and lighter penalties under the New Income Tax Act, 2025, which will come into effect from April.

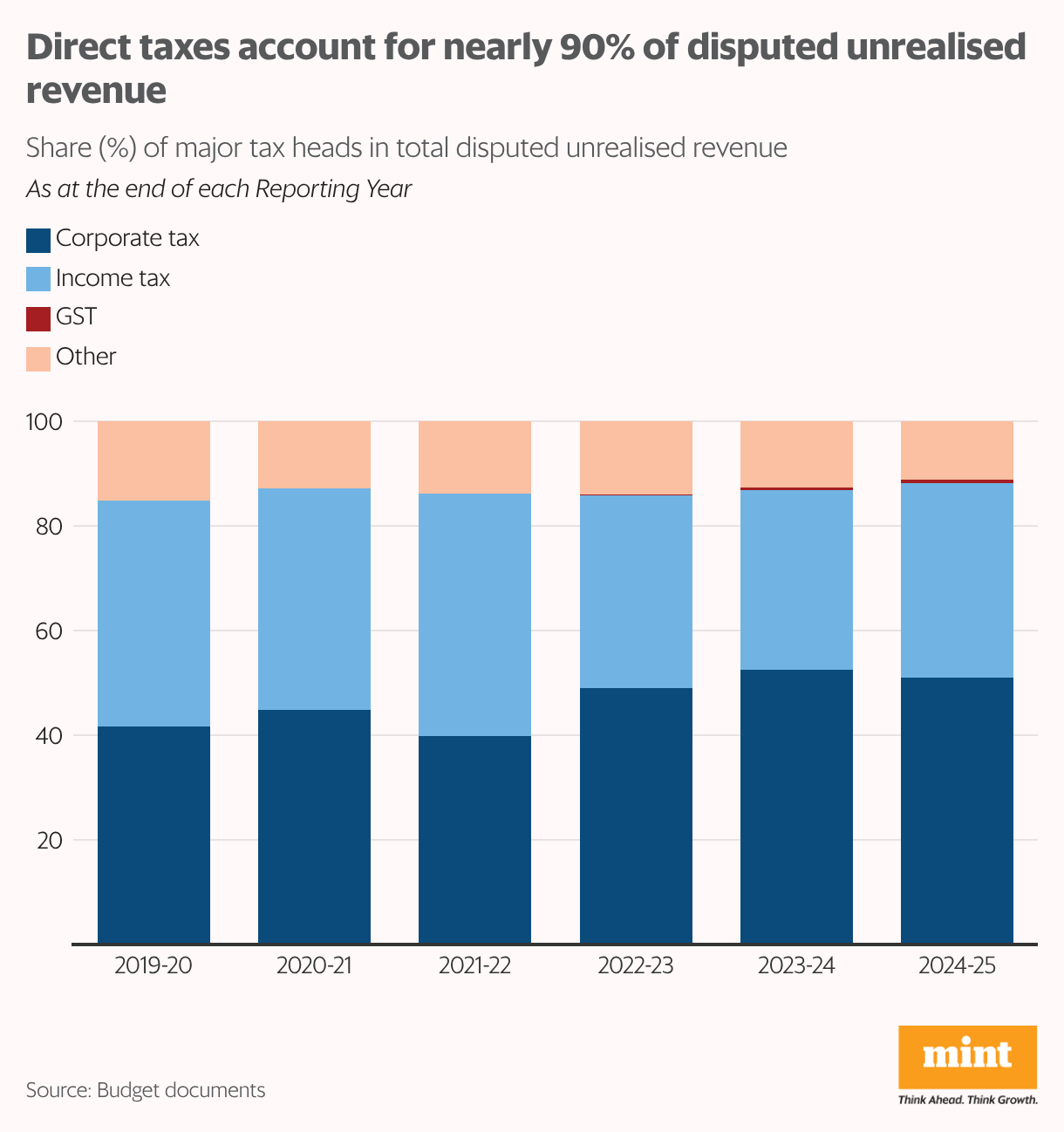

Within the disputed amount, corporate taxes still account for the lion’s share – 51% in FY25 – while income taxes account for 37%. The share of income tax under dispute has fallen below 40% since FY23.

The share for corporate taxes has risen to more than 50% since FY24. Experts say a steady rise in the number of insolvency and bankruptcy cases has hindered the state’s ability to enforce and realize assessed taxes over the years. Data from the Insolvency and Bankruptcy Board of India (IBBI) show that insolvency initiations have risen sharply over the past decade, from just 37 cases in FY17 to 733 in FY25.