How the India-EU FTA redraws the luxury car market

For EU-built cars priced above €15,000 ( ₹16.40 lakh), tariffs are expected to ease in stages, starting at around 30-35% when the pact takes effect, likely by the end of 2026. This will further fall to 10% over the next five years, depending on the segment. This could gradually open up India’s luxury car market.

A small pie with big potential

Lower tariffs make it easier and cheaper for global brands to import premium and niche models. That said, luxury vehicles still account for only a very small share of the overall market. In 2025, luxury car sales were estimated at about 53,000 units, a small pie of India’s total passenger vehicle (PV) volume of 41,53,432 units.

This FTA could help expand the luxury segment’s reach over the long term, especially as the premiumization trend has gained traction. Within this shift, Landmark Cars appears well placed to benefit, with its share price rising 15% following the announcement. This article explains why.

Mercedes accounts for 39% of Landmark’s revenue

Landmark Cars has a roughly 0.5% volume share and 0.8% value share in the overall passenger vehicle market. It is India’s leading premium automotive retail platform and the country’s first publicly listed, multi-brand automobile retailer. It is a preferred retail partner for a wide range of original equipment manufacturers across the premium and luxury vehicle segments.

![[ Insert title here ] (Bar Chart)](https://datawrapper.dwcdn.net/7Mk7w/full.png)

This gives Landmark a diversified presence within the Indian automotive retail ecosystem. A key aspect of this portfolio is its exposure to European Union (EU) brands, including Mercedes-Benz, Volkswagen, Renault, and Citroën. In fact, among these, Mercedes alone accounted for 39% of Landmark’s top line in H1 FY26. A higher share of luxury models is also reflected in Landmark’s average selling price (ASP) of ₹23.16 lakh.

This suggests that the increased penetration of premium vehicles, aided by the India-EU FTA, could directly benefit the company. Beyond its EU exposure, Landmark also has partnerships with Honda, Jeep, BYD, Kia, M&M, and MG Motor. It is the largest retail partner in India for Mercedes, Volkswagen, BYD, Honda, and Jeep, giving it scale across luxury and mass-market segments.

As of November 2025, the company operated 139 outlets, comprising 75 sales showrooms and 64 workshops, across 29 cities in 12 states. Landmark has actively consolidated the fragmented dealership landscape through acquisitions, with nearly a quarter of its outlets added through inorganic expansion, helping drive scale and operating leverage.

Business model: Agency versus dealership

For Mercedes-Benz, the company operates under an agency model. Under this model, customers place orders directly with Mercedes-Benz India. And Landmark acts as an agent, facilitating sales and delivery. Under this arrangement, Landmark books only the commission earned on each sale.

This results in lower reported revenue than a dealership model and reduces inventory risk and working capital requirements. For other brands, it operates under a dealership model. Under this structure, it purchases vehicles from the OEM, holds inventory, and sells directly to customers. Accordingly, the company recognizes the full invoice value of the vehicle as revenue.

Why BYD volumes tripled in just 12 months

In the proforma-revenue mix, in H1FY26, Mercedes contributed (39%), followed by BYD (10%), MG (9%), Volkswagen (8%), Honda (8%), and M&M (6%), among others. New partners (BYD, MG, M&M, and Kia) are becoming more meaningful contributors. Among these, BYD volumes have grown nearly 3X over the last year, reflecting rising demand for its electric vehicle portfolio.

In the pro forma, Mercedes sales are treated as gross rather than commission-based. Beyond new-vehicle sales, Landmark also offers after-sales service, pre-owned vehicle sales, and the distribution of third-party finance and insurance products. This integrated operating model enables Landmark to capture value across the entire vehicle ownership lifecycle. This reduces its dependence on new-vehicle sales and partially cushions it from cyclical demand fluctuations.

Strong revenue growth but weaker profitability

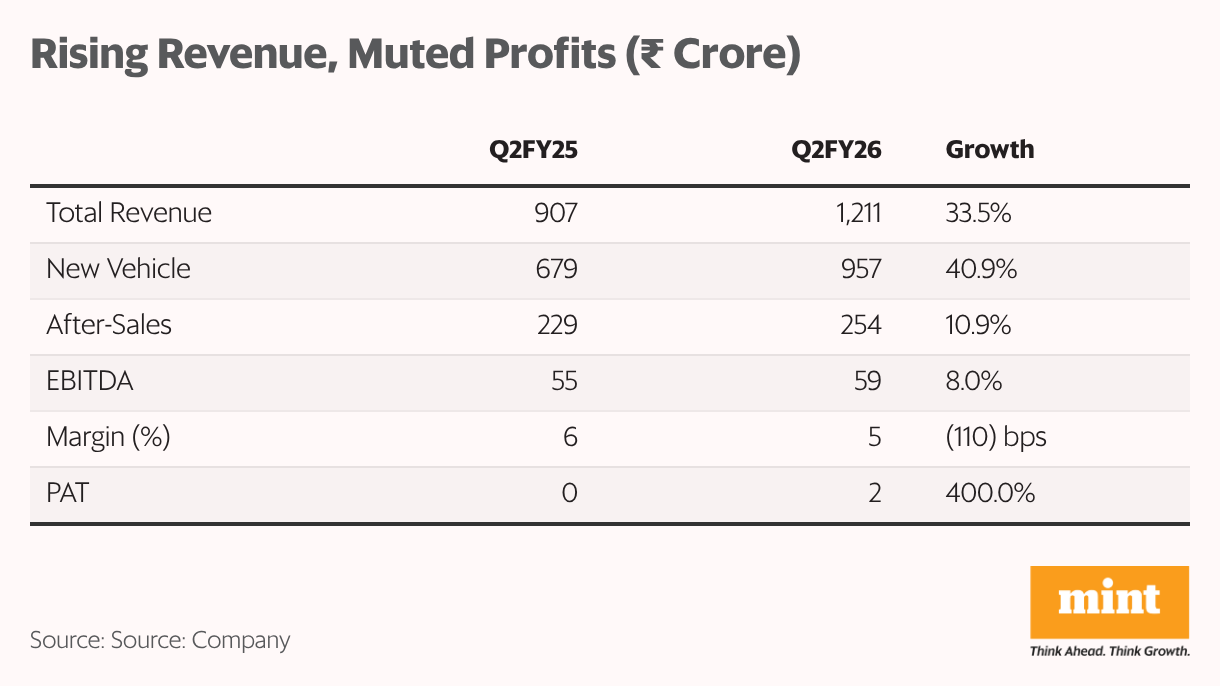

Within this structure, new vehicle sales remain the largest revenue contributor. This includes both outright vehicle sales and commission income from the Mercedes. Reported revenue from this segment increased 40.9% year-on-year to ₹₹956.8 crore in Q2FY26, accounting for 79% of top line.

This was supported by a 14.7% rise in ASP to ₹23.16 lakh, driven by a favorable mix skewed towards higher-end models, particularly Mercedes-Benz. The remaining came from After-sales, whose revenue increased 10.9% to ₹254 crore in Q2FY26. However, this segment is currently driving profitability, with a margin of 16.1% (down from 18.8% in Q2FY25), compared with 1.4% for new vehicle sales.

At a consolidated level, revenue grew 33.5% year-on-year to ₹1,211 crore in Q2FY26. EBITDA grew by 8% to ₹59.2 crore, while margin moderated to 4.9% from 6.0% in Q2FY25. This was partly due to stock liquidation driven by the GST rate cut and the slower ramp-up of new stores. Net profit surged to ₹1.5 crore, albeit from a low base of ₹30 lakh in Q2FY25.

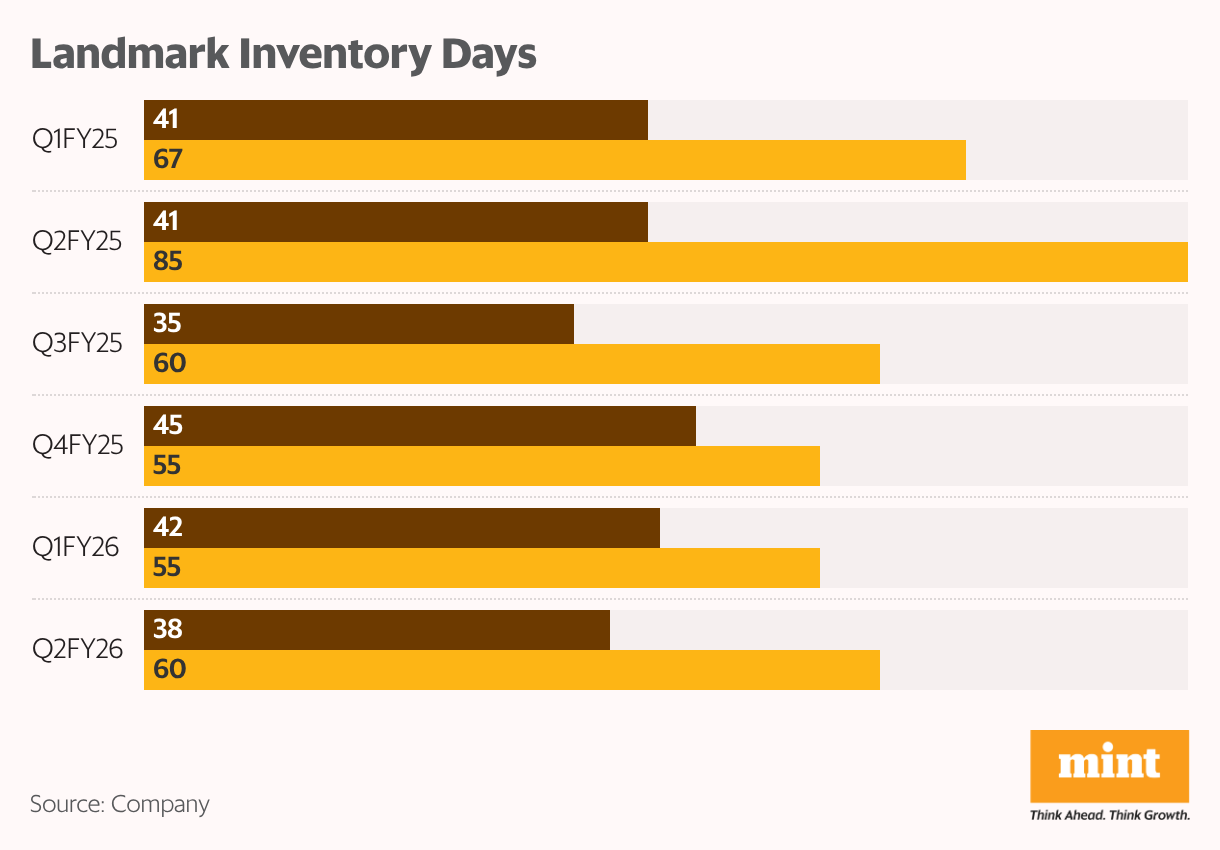

Also, Landmark leads the industry in inventory discipline, with inventory days of 38, well below the industry average of 60 days, reflecting faster sales conversion. With net cash from operating activities of ₹177 crore in H1FY26, the company continues to generate positive operating cash flows even amid an aggressive expansion and growth phase.

Ramping up 23 new outlets

The company plans to accelerate revenue growth and restore profitability as operating leverage increases. It’s because Landmark aggressively opened 23 new outlets in FY25, which are yet to break even. Management highlighted that new loss-making outlets in Q2 are expected to break even by the end of FY26.

At this stage, the company also does not plan any major organic additions, such as new outlets or workshops. The focus has shifted to stabilizing and ramping up recently opened locations, allowing them to mature and move toward optimal utilization levels. This should support profitability and margin.

GST cut is a key demand catalyst

Management believes the Indian passenger vehicle market has entered a faster phase of recovery following the GST rate reduction and expects further demand support from potential interest rate cuts. October registrations grew at a double-digit pace, reaching close to 5.5 lakh vehicles, while inquiry levels in the first 10 days of November were around 20% higher than last year.

The longer-term outlook is supported by expansion plans from key OEM partners. Honda has outlined plans to scale volumes 5X over the next five years, supported by the launch of 10 new models by 2030. Beyond BYD, Mercedes is preparing a broad product rollout beginning in 2026, while Renault is also expected to re-enter the SUV segment with the recent launch of the new Duster.

Landmark views the current structure of the Indian automotive retail market as an opportunity for consolidation. The company aims to double its market share over the medium term through a mix of organic and inorganic growth. The India-EU FTA could play a decisive role in expanding the share.

At ₹395, Landmark is trading at an EV/EBITDA multiple of 9.5, a discount to its smaller peer, Popular Vehicles (12.1). That said, Landmark’s profitability trend has been weaker, with margins remaining uneven across cycles. This makes improving profitability, driven by tighter execution and better operating leverage, a key area to watch. Cyclicality in the automobile sector remains a key risk.

For more such analysis, read Profit Pulse

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. This is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.