Meanwhile, this earnings season has thrown up an interesting development—a set of businesses whose financial turnarounds have arrived just as the market’s mood has improved. That synchronization matters. When profits turn after a stock has already rerated, the payoff is limited. But when operational improvement coincides with a sentiment shift, markets tend to respond disproportionately.

That is the narrow lens of this piece. Focusing on three businesses where profitability has returned in Q3FY26 through genuine operating leverage and cost discipline, not accounting creativity, let us examine how fundamentals and risks stack up against stock prices at this inflexion point.

JSW Cement: Cost-leadership bore fruit

The JSW Cement stock rallied over 9% on Thursday after the company reported a smart turnaround into profits in the December quarter. Despite exceptional expenses ₹34 crore on account of the new labor codes, the company went from reporting an ₹80 crore loss in Q3FY25 to ₹131 crore profits in Q3FY26.

Recovering from a weak demand environment, particularly in JSW’s mainstay southern and eastern markets, the company’s intrinsic cost advantage is finally playing to its favour. The lowest clinker factor in the industry at about 50% enables low fuel and energy consumption at JSW, even as its high 40% share of GGBS (ground granulated blast furnace slag) in its output has helped expand margins.

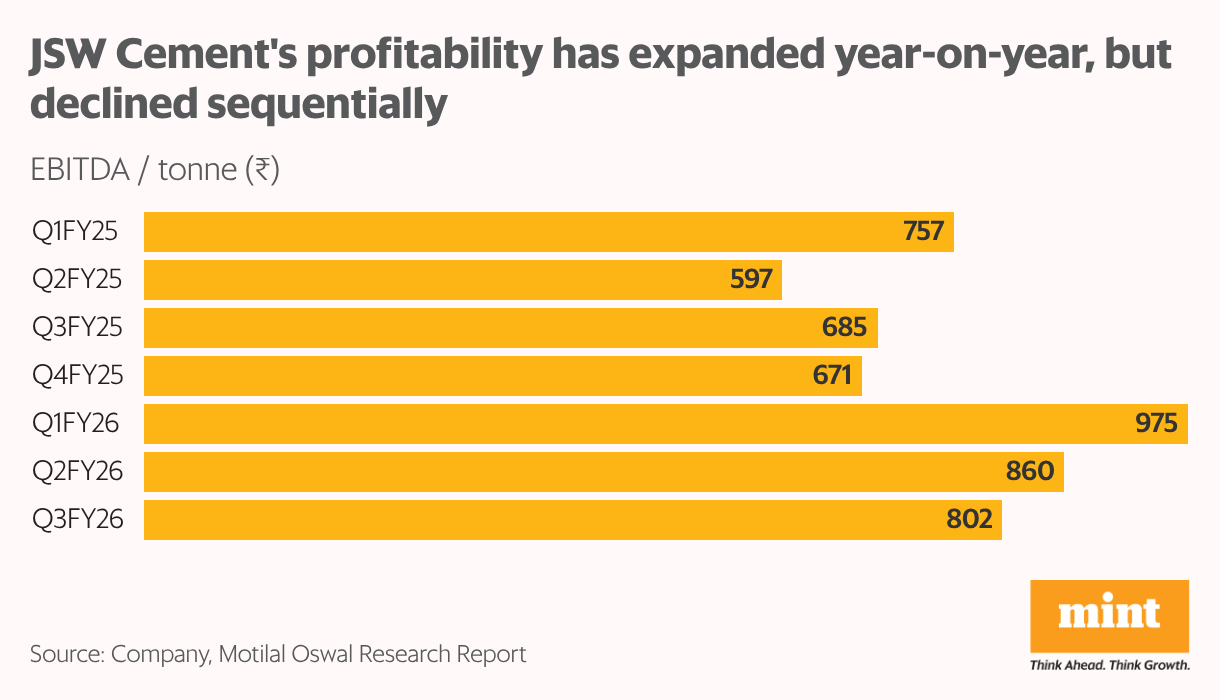

Growing premiumization of its product-mix, higher use of green power that is expected to triple to 63% by FY27, and logistics optimization are expected to expand Ebitda/tonne from ₹802 in Q3FY26 to over ₹1,000 by FY28.

Capacity is slated to expand from 22 million tonnes per annum (mtpa) to 34mtpa by 2028, and to 42mtpa thereafter, paving the way for growth, while also diversifying geographical risk beyond South India. The flip side of the coin, however, is that the debt-funded expansion can undo the progress made on net-debt reduction post its IPO. Net debt-to-Ebitda stood at 2.9x in the December quarter.

Meanwhile, delays in regulatory approvals for expansion and pricing pressures amid intense competition can make matters worse. The writing is already on the wall with the sequential decline in realizations during Q3FY26. Free cash flows may also turn intermittently negative, weighed down by investing cash outflows. That said, with the stock now trading above its critical support of ₹120 apiece, if the promising profitability trends sustain, there is room for further appreciation.

Pine Labs: Post-IPO profitability turnaround fails to lift sentiment

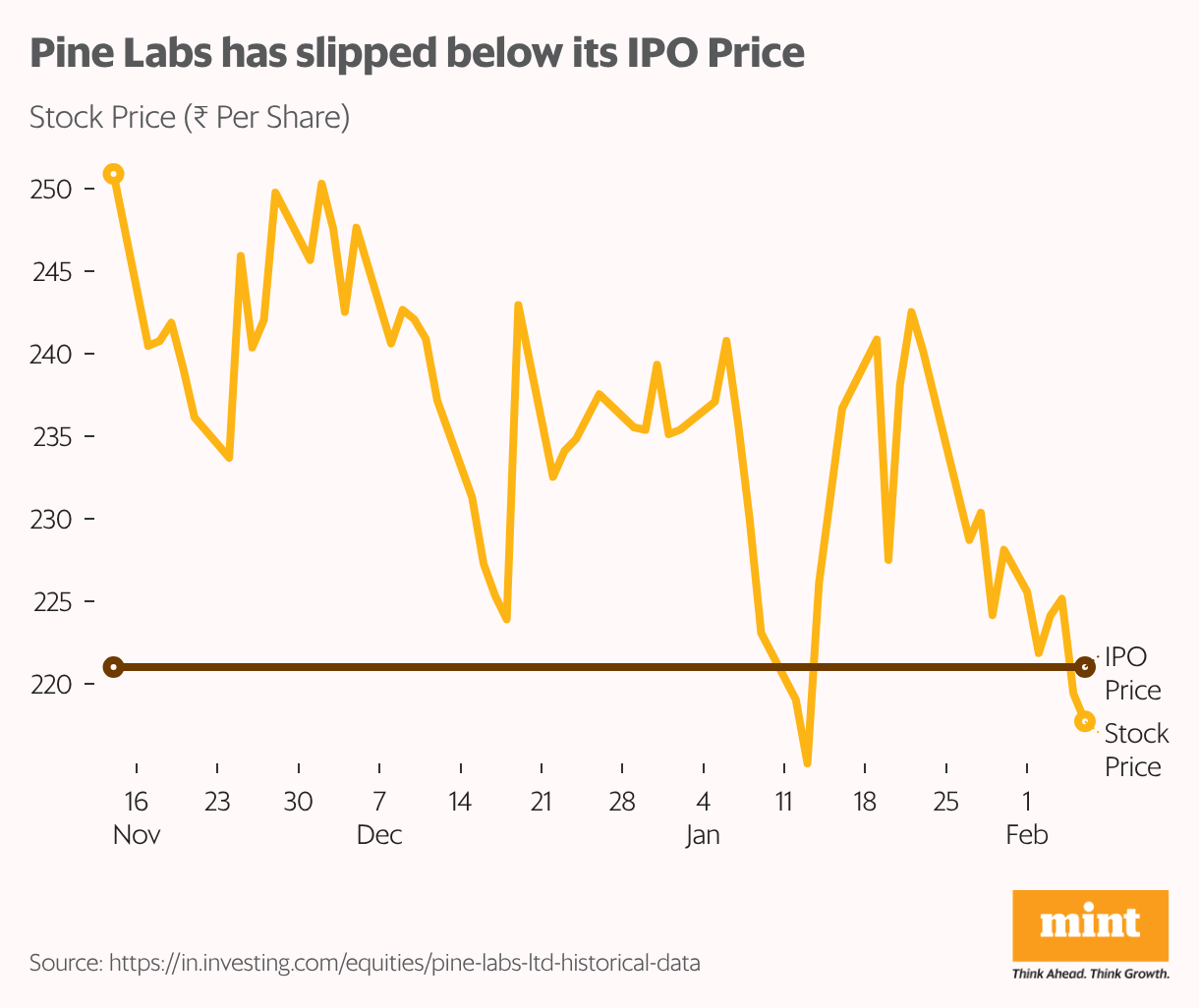

Fintech firm Pine Labs had listed in early November 2025 at a premium of almost 10% to its IPO price. Since then, amid pessimism in the broader market, increased caution has caused the stock to tumble back below its IPO price.

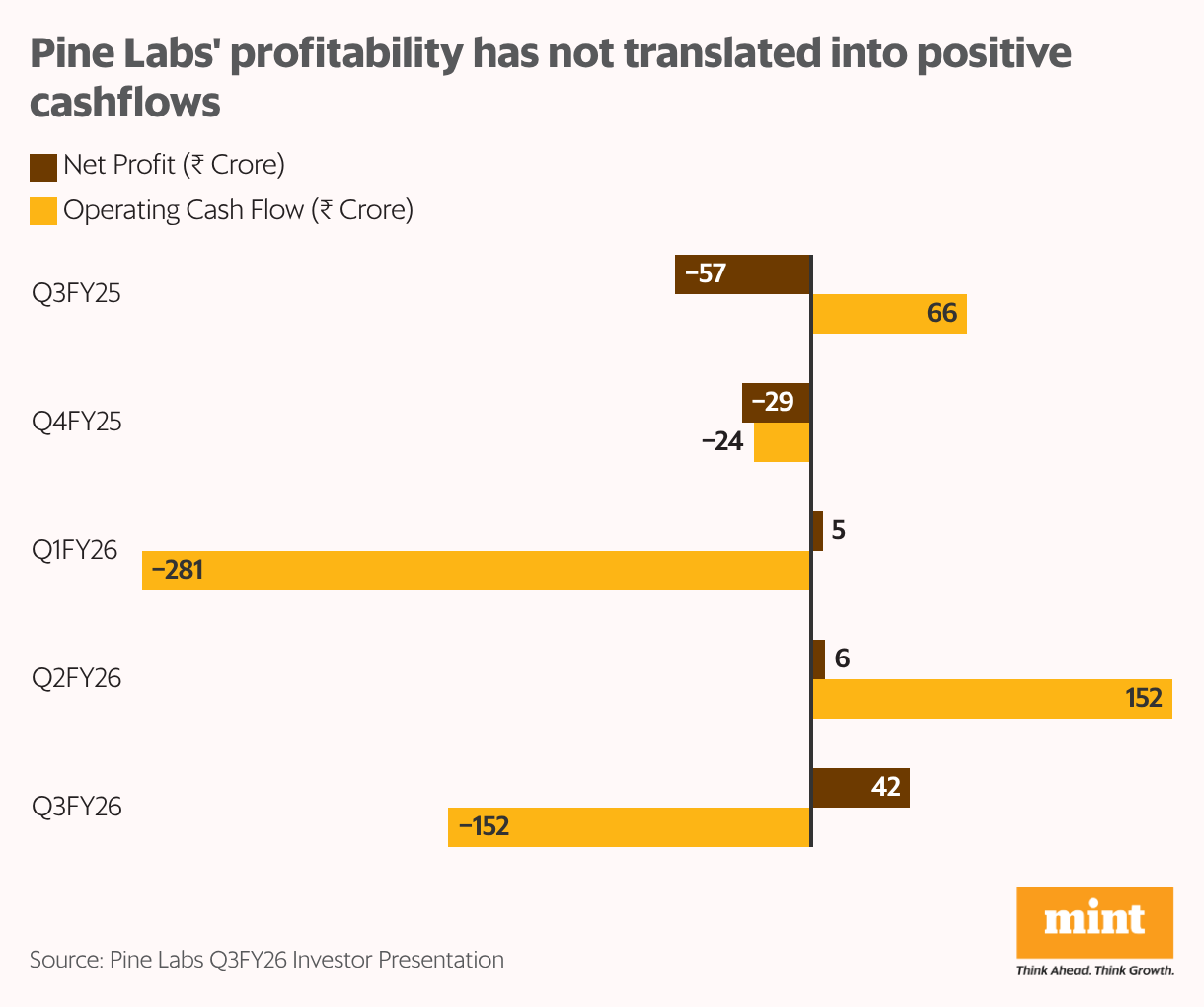

Even a turnaround into profitability during the December quarter has not been able to lift investor sentiment. despite reporting ₹42 crore in profit during Q3FY26, a massive recovery from the ₹57 crore loss in the year-ago period, the stock has corrected over 5% since the earnings announcement on 28 January. What gives?

Pine Labs clocked 29% growth in its gross transaction value to ₹4.5 trillion, driven by the higher-margin software-led revenues. Lower drags from depreciation and Esops also supported margins, more than offsetting the ₹10 crore additional costs incurred on account of the new labor codes.

But investors are looking beyond the recently reported profitability, particularly since Q3’s profits did not translate into cash flows. Weighed down by high working capital, Pine Labs continued to report intermittently negative operating cash flows. Competition is also rife in the industry, with PhonePe also gearing up for its IPO. Razorpay, PayU, and Google Pay also command considerable market and mindshare in the online acquiring/gateway and BNPL (buy now, pay later) segments, and can affect Pine Labs’ pricing power and margins going forward.

Mixed regulatory signals, possibly on BNP lending, can also play spoilsport. We had recently witnessed Pine Labs’ growth affected by confusion around the GST payable on gift card sales. The growing share of international revenues also poses a risk, considering that international take rates are lower for issuers or processors like Pine Labs vs distributors.

Pine Labs is also exposed to partner-concentration risk. Losing large bank or retail partnerships can weigh significantly on its fortunes, which is the flip side of being a smaller firm partnering with the top banks, petrol companies, retailers, and ecommerce and quick-commerce players. The firm’s transition into an asset-light business also warrants close monitoring of execution and top-line growth, given that the pivoted focus from hardware-led towards software-led revenues.

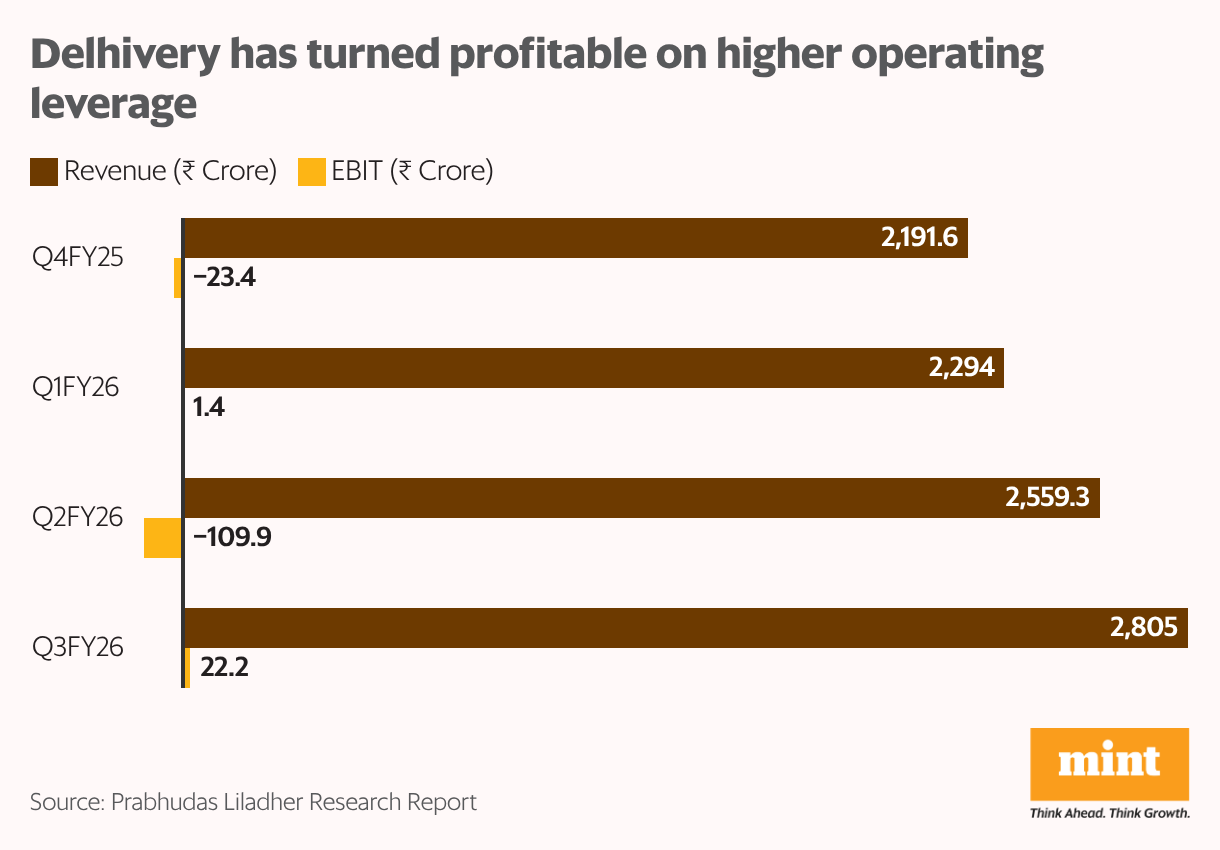

Delhivery: Volumes drove profitability

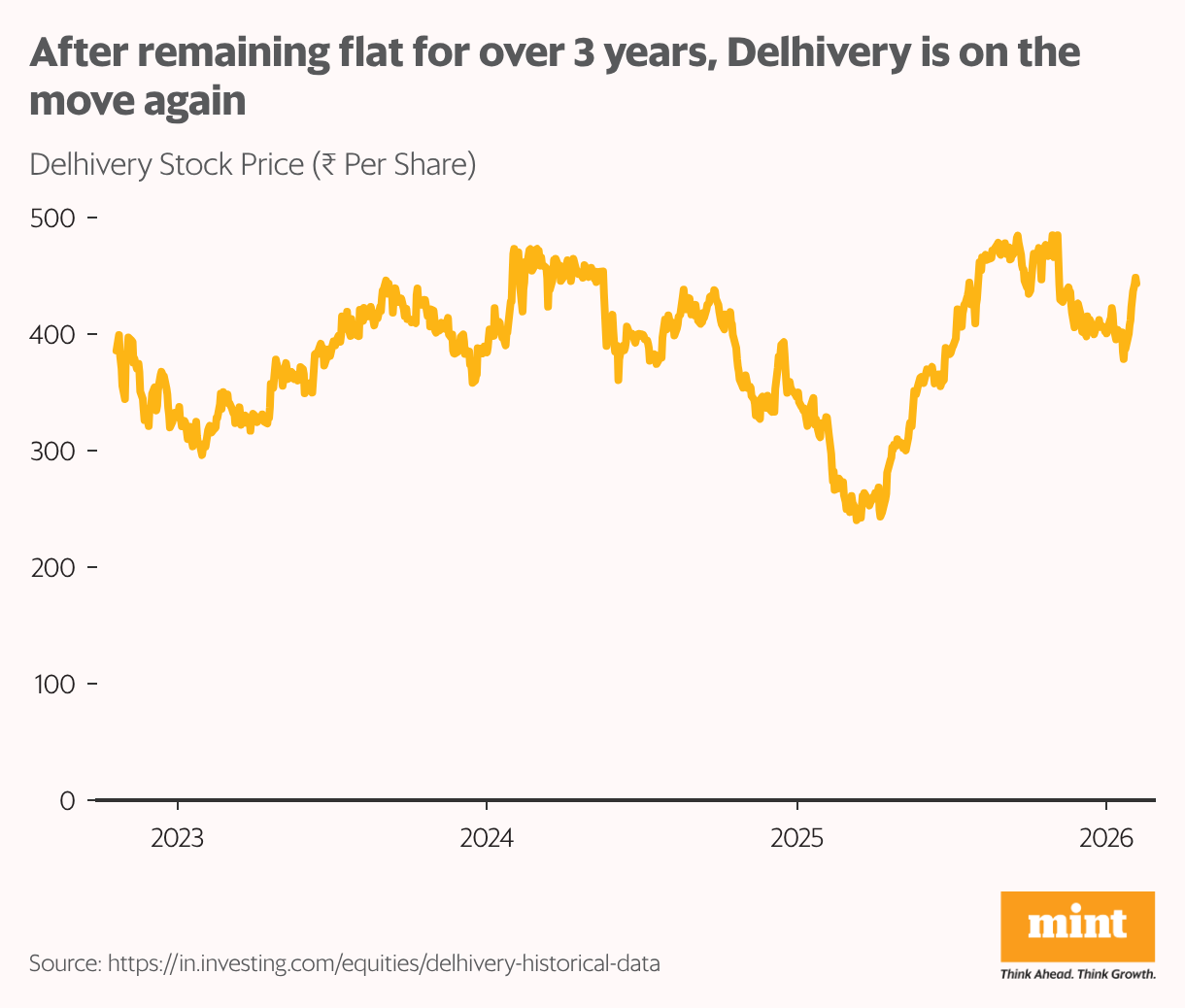

Investors in Delhivery have cheered the business developments even ahead of its earnings announcement a few days ago. Anticipating the turnaround into profitability, the stock rallied almost 15% in less than two weeks. To be sure, this came after subdued sentiment for over three years.

While integration expenses related to the E-Com Express acquisition added ₹35 crore to Delhivery’s costs during the December quarter, operating leverage and margins received a big push from an impressive 43% year-on-year increase in parcel volumes. Supported further by a growing share of margin-accretive e-commerce, its service EBITDA margin clocked a record high during the quarter.

Adjusted EBITDA margin came in at 5.2%, and the management has guided for free cash-flow breakeven at a margin of 6%. But its margin-trajectory hinges on the successful execution of its E-Com Express acquisition, especially against the context of year-on-year moderation in B2C per-shipment realizations amid intensifying competition. Ebit margins will also need to be closely tracked, as organic and inorganic expansion can add to depreciation costs.

That said, if and when the acquisition synergies accrue, volumes and margins stand to gain ground, buoyed by network densification, scale benefits, potentially higher pricing power, and cross-selling opportunities into new growth adjacencies. This will be a welcome development for the stock trading at almost 200x P/E. If it sustains above ₹400 apiece, the technical indicators can sync up with the fundamental turnaround and drive earnings upgrades.

Caveats

When corporate results no longer lag sentiment but sync with it, it is when guarded optimism turns into a durable re-rating. But a headline profit or sequential bounce does not guarantee sustained improvement. A deep dive matters, and the key questions to ask are: Are the earnings durable? Are the revenue drivers repeatable? Is the margin expansion sustainable? Does the balance sheet back up the turnaround? Risks always remain, but if the risk-reward appears promising, the investment can yield multibagger returns.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment advisor.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.