As a result, rather than embracing across-the-board liberalization, nations increasingly rely on bilateral and regional trade agreements, often shielding sensitive domestic sectors. The shift has intensified during the Trump years, with tariffs used as tools of geopolitical leverage and countries scrambling to secure preferential access. India too has signed a flurry of agreements, including those with the EU and the US.

While FTAs today are increasingly driven by geopolitical and supply-chain considerations, past experience shows they deliver results only when backed by competitiveness, infrastructure and domestic reforms.

Protectionist pressures

The ratio of global goods trade to GDP, which peaked at 51% before the global financial crisis, has remained broadly stable over the past decade, fluctuating between 41% and 48%.

Even after shocks such as the covid pandemic and Russia’s invasion of Ukraine, trade flows did not collapse. Firms rerouted supply chains, diversified sourcing and found new markets, keeping global commerce resilient despite geopolitical tensions. While the world economy is not closing its doors just yet, fault lines have been deepening since Donald Trump took office for a second term in January 2025.

A WTO analysis shows that the trade coverage of import-related measures implemented between October 2024 and October 2025 surged to $2.64 trillion, accounting for 11.1% of world imports, more than four times the $611 billion recorded a year earlier.

Trump has increasingly deployed tariffs as geopolitical tools, justified on grounds ranging from correcting historical trade deficits to addressing national and international security concerns. India, for instance, faced 25% penalty tariffs over its Russian oil purchases. Striking trade agreements in this landscape is less about textbook efficiency gains and more about securing supply chains, reducing policy uncertainty and insulating exports from weaponised tariffs.

power blocks

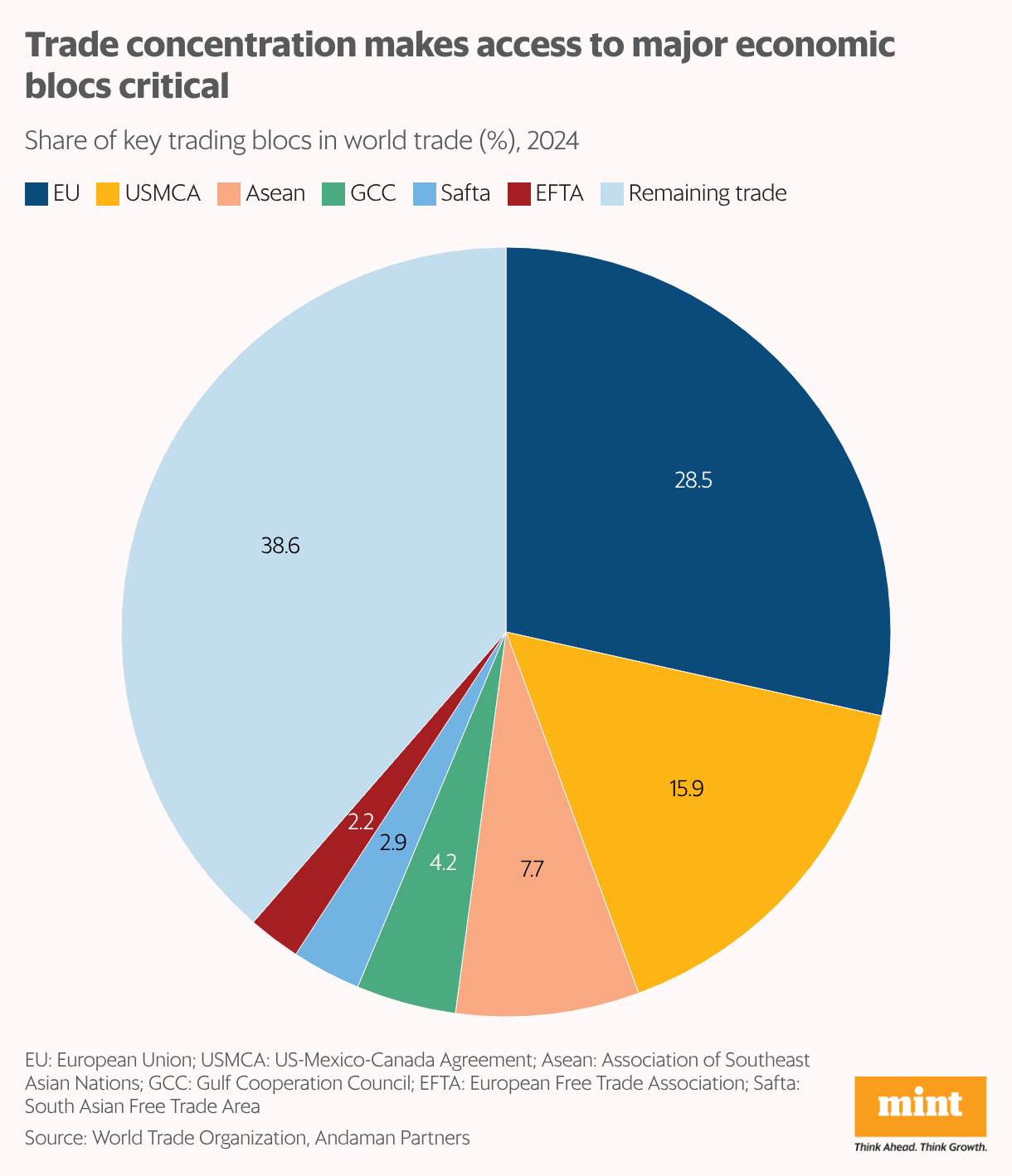

Cross-border trade is heavily concentrated in a handful of large economic blocs. Just six trading groupings account for roughly 60% of global merchandise exports and imports.

The European Union (EU), United States-Mexico-Canada Agreement (USMCA) and Association of Southeast Asian Nations (Asean) together command more than half of world trade. These blocs increasingly set standards, shape supply chains and influence the direction of capital flows, making access to them critical for export-oriented economies.

Further, while overall global trade growth slows during crises, intra-bloc trade tends to remain relatively resilient. A study by the International Monetary Fund (IMF) shows that in the period following Russia’s invasion of Ukraine, average quarterly trade growth between geopolitically distant blocs was nearly 5 percentage points lower than in the pre-war years. By contrast, trade within blocs recorded a much smaller decline of around 2 percentage points. Investment patterns show a similar tilt towards partners within established groupings.

For countries, remaining outside large trade arrangements, therefore, carries tangible risks. Exporters may face higher barriers and investment may shift to competitors enjoying preferential access. Being part of major arrangements, by contrast, offers insulation, predictability and assured market access.

rare success

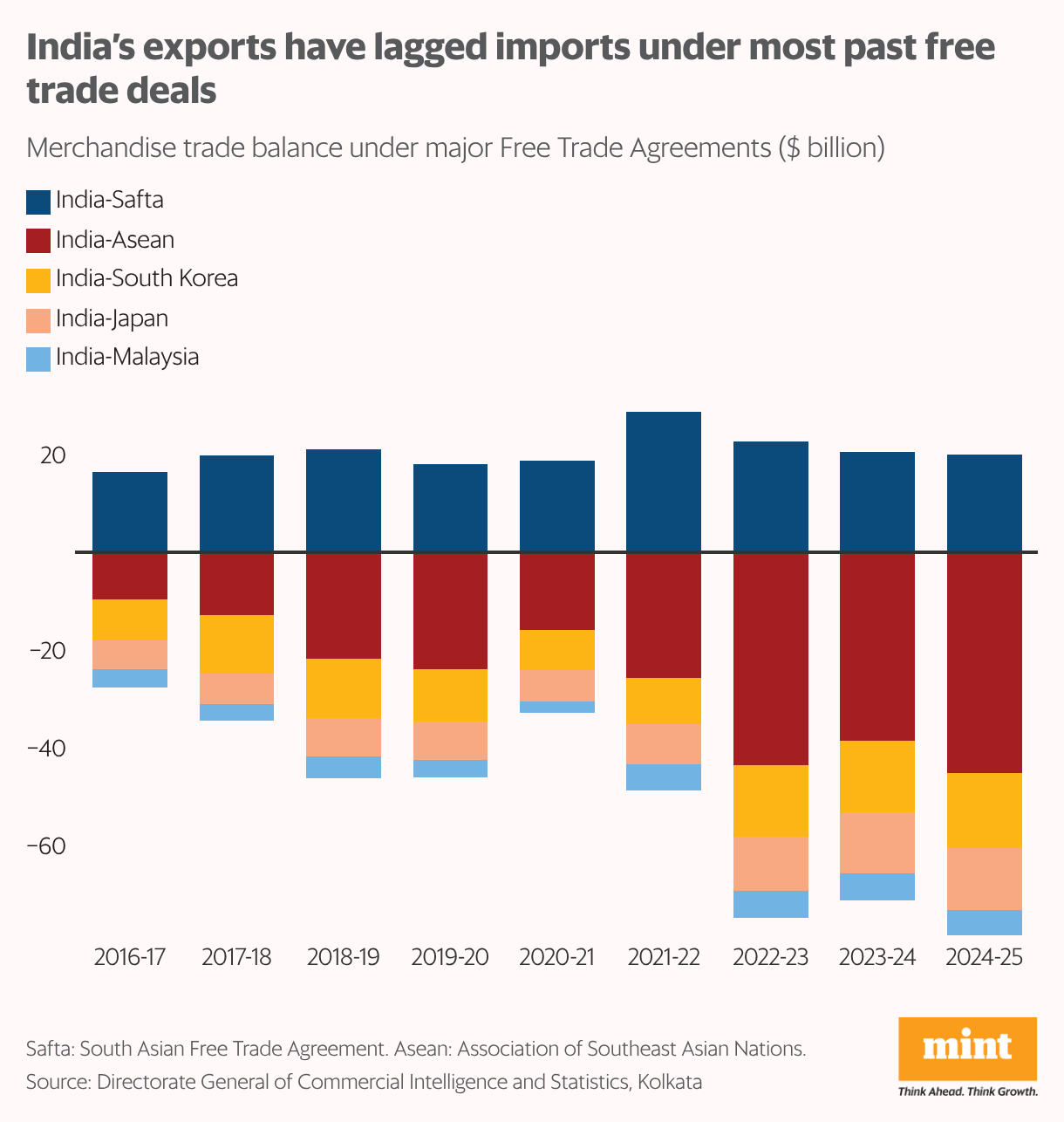

While trade deals may be the need of the hour, India’s past experience with FTAs has been underwhelming. Among the major agreements signed earlier, only the South Asian Free Trade Agreement (Safta) with South Asian Association for Regional Cooperation (SAARC) nations has delivered a trade surplus. In most other cases, India has ended up buying far more from its FTA partners than it sells to them.

According to NITI Aayog, India’s exports to FTA partner countries stood at $38 billion in July-September 2025, while imports surged to $69.8 billion, leaving a trade deficit of $31.8 billion. recent Every quarter has seen imports outpace exports, steadily widening the gap.

Import growth has been driven by higher inflows from Asean, Safta nations, Japan, Thailand and Singapore. These shipments largely comprise energy products, machinery, electronics components and chemicals, which are critical inputs that domestic industry cannot fully supply. By contrast, exports to key FTA markets such as Asean, Malaysia and Singapore have contracted sharply, with only a few destinations posting modest gains.

Thus, while tariff cuts have made partner-country goods cheaper in India, spurring imports of intermediates and fuels, export gains have lagged, reflecting limited integration into global value chains and weaker manufacturing competitiveness.

Hidden hurdles

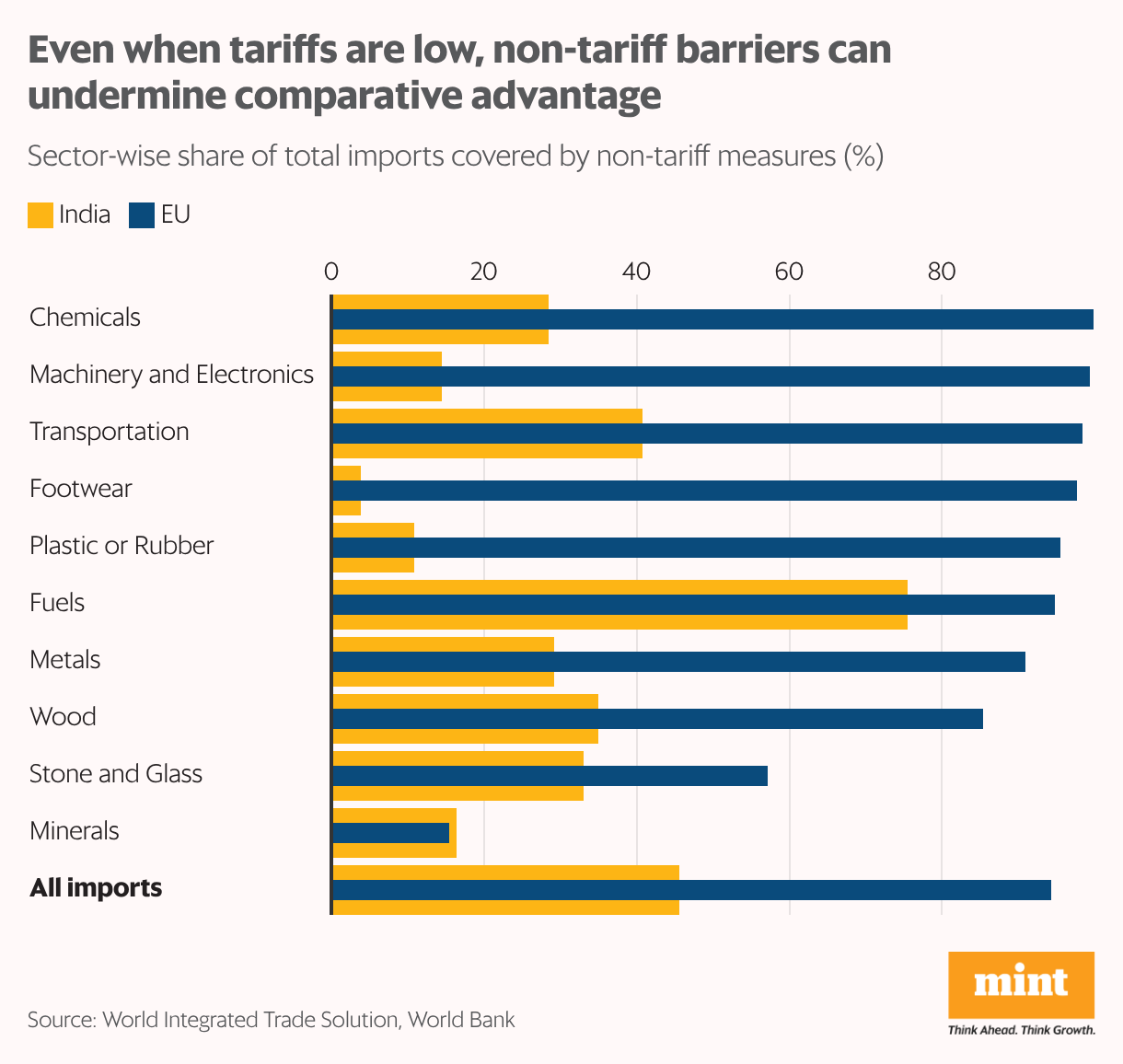

Most trade agreements focus on cutting tariffs, but duties are only part of the story. Non-tariff measures (NTMs) often matter just as much. These include product standards, technical regulations, sanitary and phytosanitary rules, licensing requirements, quotas, environmental norms, and testing and certification procedures. While many are introduced for legitimate reasons such as safety or sustainability, they can raise compliance costs and slow market access.

The India-EU FTA is a case in point. Under the finalized deal, India will eliminate duties on 93% of EU imports by value, while the EU will do so for 99% of Indian exports. On paper, this signals deep tariff liberalisation. However, the EU’s import coverage of NTMs is significantly higher across most sectors. In chemicals, machinery, metals and transportation equipment, nearly the entire import basket faces NTMs in the EU, compared with much lower coverage in India.

Also, for Indian exporters, especially in steel and aluminium, the EU’s Carbon Border Adjustment Mechanism imposes a carbon cost based on emissions intensity. Even if duties fall to zero, compliance with environmental standards and reporting requirements could impose substantial barriers. Market access therefore depends as much on regulatory compliance as on tariff cuts.

Manufacturing mismatch

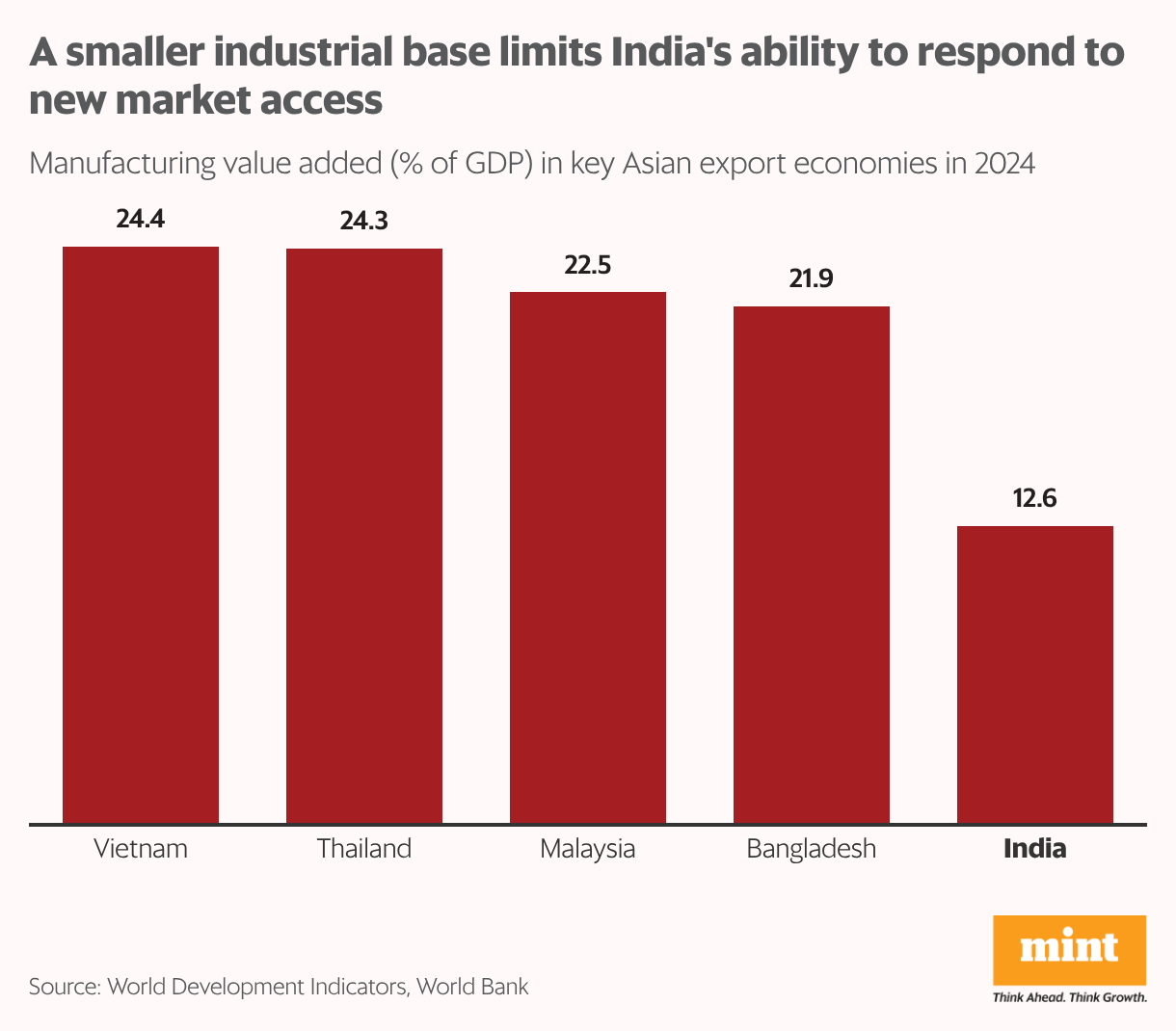

Even as new trade agreements lower tariffs and expand market access, export gains for India are not automatic. A relatively narrow manufacturing base limits the country’s ability to respond when foreign demand rises, while competitors such as China, Vietnam and Bangladesh are better positioned to seize new opportunities due to stronger and more productive manufacturing ecosystems.

Setting up factories in India remains costly and complex, given high logistics expenses, expensive and unreliable commercial power, land acquisition challenges and regulatory hurdles.

Despite initiatives such as Make in India and production-linked incentives, manufacturing momentum outside electronics has been uneven. Credit constraints persist and exports remain concentrated among a small group of large firms.

The government is now attempting to reposition Brand India in the premium global markets of the US, UK and EU by promoting heritage and high value sectors such as Banarasi and Kanchipuram silks, wellness products and select engineering goods through coordinated branding and export promotion.

Yet branding cannot substitute for competitiveness. To benefit meaningfully from new FTAs, India must deepen manufacturing capability, improve infrastructure and logistics, and widen the base of exporters. Without addressing these structural bottlenecks, market access alone may not translate into sustained export expansion.

Puneet Kumar Arora is assistant professor of economics at Delhi Technological University. Jaydeep Mukherjee is professor of economics at Great Lakes Institute of Management, Chennai.